To modify Benjamin Franklin, it seems that in Australia nothing can be said to be certain, except death, taxes and endless debate about property prices. Why is it so unaffordable? Are foreigners to blame? Is it a good investment? Is negative gearing the problem? Are property prices about to crash?

Worries about a property crash have been common since early last decade. In 2004, The Economist magazine described Australia as “America’s ugly sister” thanks in part to a “borrowing binge” and soaring property prices which had seen it become “another hotbed of irrational exuberance”. At the same time the OECD estimated Australian house prices were 51.8% overvalued. Since the GFC, predictions of an imminent property crash have become more common with talk that a property crash will also crash the banks and the economy.

Our view since around 2003 has been that overvaluation and high levels of household debt leave the housing market vulnerable. As such it could be seen as Australia’s Achilles heel. However, in the absence of a trigger it’s been hard to see a property crash as a base case. Not much has really changed. This note takes a look at the key issues and what it means for investors.

Overvalued, over loved and over indebted

The two basic problems with Australian housing are that it is expensive and household debt is high. Overvaluation is evident in numerous indicators:

-

According to the 2016 Demographia Housing Affordability Survey the median multiple of house prices in cities over 1 million people to household income is 6.4 times in Australia versus 3.7 in the US and 4.6 in the UK. In Sydney it’s 12.2 times and Melbourne is 9.7 times.

-

The ratios of house prices to incomes and rents are at the high end of OECD countries and have been since 2003.

-

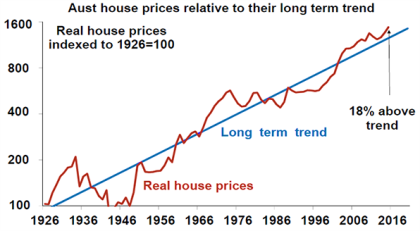

Real house prices have been above trend since 2003.

Source: ABS, AMP Capital

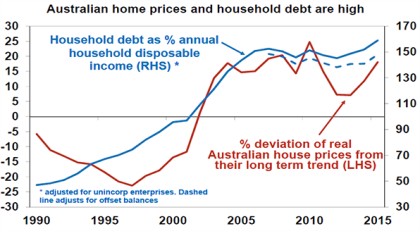

The shift to overvaluation more than a decade ago went hand in hand with a surge in the ratio of household debt to income, which took Australia’s debt to income ratio from the low end of OECD countries to now being around the top.

Source: ABS, RBA, AMP Capital

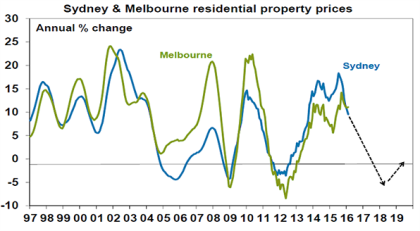

Overvaluation and high household debt are central elements of claims that Australian house prices will crash. These concerns get magnified whenever there is a cyclical surge in prices as we have seen recently in Sydney and Melbourne.

But a crash seems elusive

However, given the regularity with which crash calls for Australian property have been made over the last decade and their failure to eventuate, it’s clear it’s not as simple as it looks.

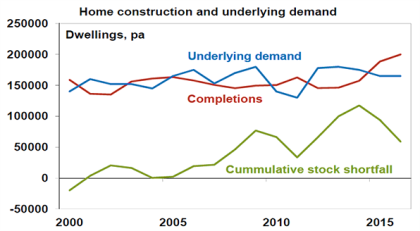

First, the main reason for the persistent “overvaluation” of Australian home prices relative to other countries is constrained supply. Until recently Australia had a chronic under supply of over 100,000 dwellings, as can be seen in the next chart that tracks housing completions versus underlying demand. Completions are at record levels but they are just catching up with the undersupply of prior years.

Source: ABS, AMP Capital

Consistent with this, vacancy rates while rising are below past cycle highs. In fact, in Sydney they are still quite low.

Source: Real Estate Institute of Australia, AMP Capital

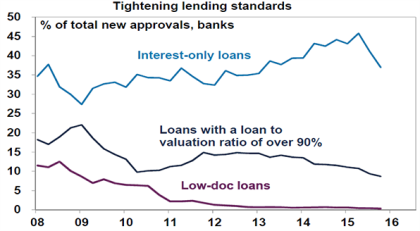

Secondly, Australia has not seen anything like the deterioration in lending standards other countries saw prior to the GFC. There has been no growth in so-called low doc and sub-prime loans which were central to the US housing crisis. In fact in recent years there has been a decline in low doc loans and a reduction in loans with high loan to valuation ratios. See the next chart. And much of the increase in debt has gone to older, wealthier Australians, who are better able to service their loans.

Source: APRA, AMP Capital

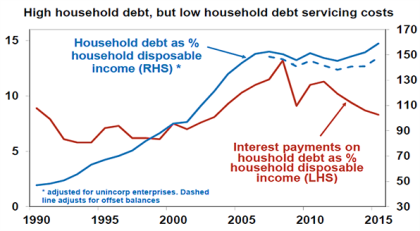

Third, and related to this, there are no significant signs of mortgage stress. Debt interest payments relative to income are low thanks to low interest rates. See the next chart.

Source: RBA, AMP Capital

By contrast in the US prior to the GFC interest rates were starting to rise. Yet in Australia bad debts and arrears are low. While new loan sizes have increased, Australians seem focussed on cutting their debt once they get it.

Finally, while some seem to think that because property prices in mining towns like Karatha are now crashing this is a sign that other cities will follow. This is non-sensensical. Property prices in mining towns surged thanks to a population influx that flowed from the mining boom. This is now reversing. Perth and Darwin are also being affected by this but to a less degree. By contrast the surge in property prices in cities like Sydney and Melbourne that occurred into early last decade predated the mining boom and their latest gains largely occurred because the end of the mining boom allowed lower interest rates.

The current state of play

Our assessment is that the boom in Sydney and Melbourne is slowing thanks in large part to APRA’s measures to slow lending to property investors. However, house price growth is likely to remain positive this year. Price growth is likely to remain negative in Perth and Darwin as the mining boom continues to unwind. Hobart & Adelaide are likely to see continued moderate property growth, but Brisbane may pick up a bit. Nationwide price falls are unlikely until the RBA starts to raise interest rates and this is unlikely before 2017. And then in the absence of a recession or rapid interest rate hikes price falls are more likely to be 5-10% as was seen in the 2009 and 2011 down cycles rather than anything worse.

Source: CoreLogic RP Data, AMP Capital

What to watch for a property crash?

To see a property crash – say a 20% average fall or more – we probably need to see one or more of the following:

-

A recession – much higher unemployment could clearly cause debt servicing problems. At this stage a recession looks unlikely though.

-

A surge in interest rates – but the RBA is not stupid; it knows households are now more sensitive to higher rates.

-

Property oversupply – this is a risk but would require the current construction boom to continue for several years.

Implications for investors

There are several implications for investors:

-

While housing has a long term role to play in investment portfolios it is looking somewhat less attractive as a medium term investment. It is expensive, offers very low income (rental) yields compared to all other assets except bank deposits and Government bonds and it’s vulnerable to possible changes to taxation arrangements around property.

-

There are pockets of value, eg in regional areas. You just have to look for them.

-

As Australians already have a high exposure to residential property (directly and via bank shares and property trusts), there is a case to maintain a decent exposure to say unhedged global shares because it could provide an offset if it turns out I am wrong and the Australian property market does have a crash.

AMP Capital Markets 2nd March 2016

About the Author

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.