Introduction

News that the Australian share market as measured by the ASX 200 index briefly slipped into bear market territory last week as defined by a 20% decline from the most recent high – which in this case was April last year – has generated much coverage and interest and understandable concern. This note takes a look at what bear markets are, how deep & long they have been and points out that they are not all of the big bad grizzly variety.

What’s a bear market?

Unfortunately there is no agreed definition of a correction versus a bear market – and certainly no “official” who makes declarations on this. My preferred approach is that a correction is limited to sharp falls, across a few months after which the rising trend in share prices resumes, taking shares back to new highs within say six months of the low. By contrast, a bear market sees falls lasting many months or years with a pattern of falling lows and highs and it takes shares a year or more to regain new highs.

A common approach is to use a 20% or more decline to delineate a bear market from a correction. Of course this is rather arbitrary – and right now it puts the ASX 200 as having entered a bear market (because it fell 20% from its high in April last year to its low last week), but not the broader All Ordinaries index which has “only” had a 19% fall. But I guess the line has to be drawn somewhere.

How long do Australian bear markets last?

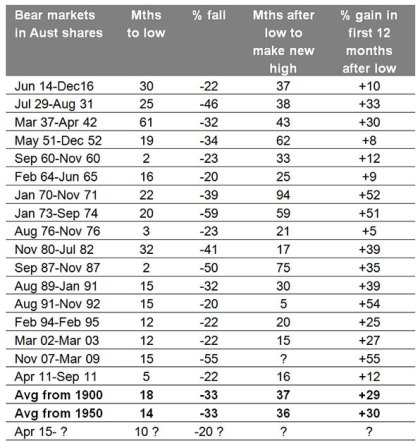

The following table shows bear markets in Australian shares since 1900 using the 20% rule.

Bear markets in Australian shares since 1900

Based on the All Ords, excepting the ASX 200 for the latest. I have defined a bear market as a 20% or greater fall in shares that is not fully reversed within 12 months. Source: Global Financial Data, Bloomberg, AMP Capital

Since 1900, Australian shares have seen 17 bear markets. These have lasted an average 18 months with an average top to bottom fall of 33%. It’s then taken an average 37 months to exceed the previous high, although we are still waiting in relation to the November 2007 to March 2009 bear market. The average gain over the first 12 months following the bear market low has been 29%, highlighting the gains that can be made up front once bear markets end.

Not all bear markets are created equal

Of course this all masks a wide range. The worst bear market was the 1973-74 slump of 59%, which lasted 20 months, as stagflation (ie recession and high inflation) took hold in the Australian economy. This was followed by the global financial crisis driven slump of 55% that lasted 15 months. The 1987 crash saw a 50% plunge over two months and the Great Crash of 1929-31 saw a 46% plunge.

At the other extreme there’ve been several bear markets of just over 20% including those of 1994-95, 2002-03 and 2011. In fact of the 17 bear markets since 1900, 11 saw shares higher a year after the initial 20% decline with an average gain of 14%. Of course the remaining 6 pushed further into bear territory with average falls over the next 12 months, after having declined by 20%, of an additional 22.5%. Stockbroker Credit Suisse, albeit focussing only on the period from the 1970s, recently called these Gummy bears and Grizzly bears respectively and since it’s a useful way to think of it I will stick to the same terminology.

Source: ASX, Global Financial Data, Bloomberg, AMP Capital

What determines how deep bear markets are?

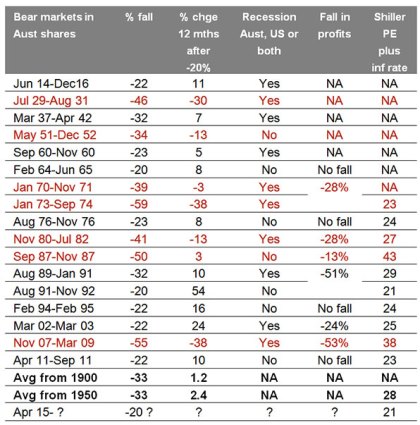

Because of the role played by investor sentiment and the risk that it can make bear markets somewhat self-feeding there is no definitive answer to this. However, the next table provides some guide. The first two columns show bear markets since 1900 and the size of their falls. The third shows the percentage change in share prices 12 months after the initial 20% decline. The fourth indicates whether they are associated with a recession in the US, Australia or both. The fifth column shows associated top to bottom falls in profits and the final column shows a measure of share market valuation at the start of bear markets. Worse than average bear markets are in red.

Contributors to the depth of bear markets in Aust shares

Based on the All Ords, excepting the ASX 200 for the latest. I have defined a bear market as a 20% or greater fall in shares that is not fully reversed within 12 months. Source: Global Financial Data, Bloomberg, AMP Capital

Several observations can be made.

First, the deeper Grizzly bear markets are invariably associated with recession, whereas the milder Gummy bear markets and even the rather short (but shocking) 1987 share market crash tend not to be. Just less than half of the Gummy bears saw a recession compared to five of the six Grizzly bears.

Second, although we don’t have earnings data prior to the 1960s, the deeper Grizzly bears tend to be associated with sharp declines in company profits, notably those of the early 1970s, early 1980s and GFC bear market. By contrast the milder bear markets such as those beginning in 1964, 1976, 1994 and 2011 often see less earnings weakness.

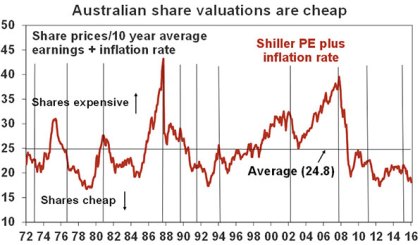

Finally, valuations are not definitive but they appear to play a role. To give a guide to valuation I have compared share prices to a rolling 10 year moving average of earnings because it corrects for cyclical swings in profits (this is referred to as the Shiller PE or cyclically adjusted PE) and then added the inflation rate to because when inflation is high PEs tend to be lower and when inflation is low PEs tend to be higher. Basically the higher this measure is the more expensive shares are. The next chart shows this measure since the 1970s with vertical lines indicating the start of bear markets. Bear markets starting in 1980, 1987, 2003 and 2007 all began with higher readings than average (24.8). Grizzly bears started with an average reading of 30 versus an average of 28 for Gummy Bears suggesting there is not much in it but that it may be factor.

Vertical lines show the start of bear markets. Source: RBA, AMP Capital

Implications for investors

Out of the 17 bear markets in Australian shares since 1900, 11 have moved higher over the 12 months following a 20% decline, suggesting that based on history there is a 65% probability that shares will move higher over the year ahead.

Factors that play a role in determining whether a much deeper bear market may occur are: whether Australia or the US have a recession, whether there is a sharp fall in earnings and albeit with less reliability valuations. In regards to these:

-

Our view remains that the US is unlikely to experience a recession given the lack of prior excesses (in terms of cyclical spending, debt growth or inflation) and the absence of significant monetary tightening.

-

In Australia, we continue to see growth tracking along at around 2.5% pa, with recent economic indicators broadly consistent with this.

-

On the earnings front, resources earnings have already crashed 80% or so and at 10% of the overall market their ability to do further damage is limited. Meanwhile, the profit reporting season underway suggests profit growth in the rest of the market is meandering along at around 5%.

-

Finally, the cyclically adjusted PE + inflation valuation measure at 21 when the current bear market started was at the low end of the range for the start of past bear markets and at 18 now is close to as low as it ever gets.

These considerations provide some hope that Australian shares will be higher rather than lower in a year’s time. The main risk is that gloom and doom about the global outlook become self-fulfilling, dragging shares lower. The historical experience suggests that there is a limit to this though and global central banks seem to be awakening to the risks and so are moving in the direction of seeking to stabilise financial conditions.

AMP Capital Markets 18th February 2016

About the Author

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.