Introduction

The past few weeks have been messy with Brexit, the Australian election, another terrorist attack in France and an attempted coup in Turkey. In fact, the last 12 months have been – starting with the latest Greek tantrum and China share market plunge a year ago. It’s almost as if someone has listened to Taylor Swift’s song “Shake It Off” and decided to try and shake up investment markets. This has all seen a rough ride in investment markets with most share markets falling into bear market territory at some point over the last year and bond yields plunging to record lows. This note reviews the worry list from the last 12 months, the impact on returns and looks at the outlook going forward.

There’s been a long worry list

The past year has seen a long worry list with:

-

Another Greek tantrum in June-July last year;

-

A 49% plunge in Chinese shares with worries about debt, growth & capital outflows as the Renminbi was devalued;

-

An ongoing collapse in commodity prices;

-

Intensifying concerns about deflation;

-

Recession in Brazil and Russia and concerns about a new emerging market debt crisis;

-

Worries about energy producers defaulting on their loans;

-

Ongoing angst about the end of the mining boom and the risk of a property crash in Australia;

-

A slump in manufacturing globally led by the US & China;

-

Concerns that the Fed raising rates and causing a further surge in the $US would accentuate problems for China, the emerging world and commodity prices;

-

Another soft start to the year for US growth;

-

Falling profits in the US, Australia and most regions;

-

Numerous IS related terrorist attacks;

-

A “surprise” vote by the UK to Leave the European Union setting of a new round of fears that there will be a domino effect of countries seeking to leave the Eurozone;

-

A messy election result in Australia with likely an even more difficult Senate which will make it even harder for the Government to control spending and implement reforms;

-

An escalation of tensions in the South China Sea; and

-

An attempted coup in Turkey.

The success of Donald Trump in the US, the Brexit vote & the close election in Australia highlight a growing angst at rising inequality and a loss of support for the economic rationalist policies of globalisation, deregulation and privatisation. While understandable, the resultant populist policy push risks slower long term economic growth and lower investment returns.

Constrained and uneven returns

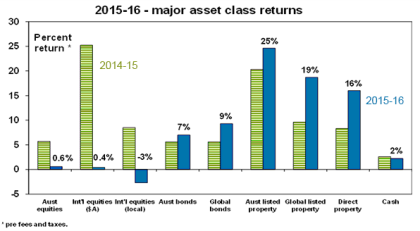

The turmoil over the last 12 months has shown up in very messy share markets (with most falling into bear market territory with 20% plus falls from last year’s highs to their lows early this year before a rebound) and a sharp decline in bond yields to record lows. However, unlisted assets like commercial property, infrastructure and listed yield-based plays like real estate investment trusts have done very well. Reflecting the constrained environment, balanced growth superannuation funds saw average returns of around 1-2%.

Source: Thomson Reuters, AMP Capital

Nine reasons why it’s not all that bad

But while super funds had soft returns over the last year they were not disastrous and moreover they averaged 8-9% over the last three years – which is not bad given how low inflation is. What’s more, while the worry list may seem high that has been the story of the last few years now. For example, 2014-15 saw worries about the end of the US Fed’s quantitative easing program, Ukraine, the IS terror threat, Ebola, deflation, a soft start to 2015 for US growth (we hear that one a lot!), worries about China, soft Eurozone growth and on-going noise about a property crash/ recession in Australia. So nothing new really! More fundamentally there are nine reasons for optimism.

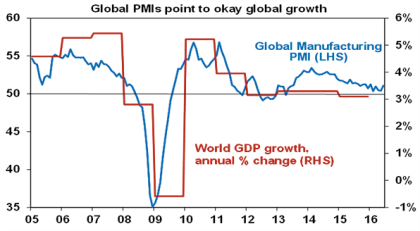

First, global growth is okay – there has been no sign of the much feared global recession. Global business conditions surveys point to ongoing global growth of around 3%.

The shift to overvaluation more than a decade ago went hand in hand with a surge in the ratio of household debt to income, which took Australia’s debt to income ratio from the low end of OECD countries to now being around the top.

Source: Bloomberg, AMP Capital

In Australia, growth has in fact been particularly good at around 3%. The economy has rebalanced away from a reliance on mining and it has benefitted from the third and final phase of the mining boom which has seen surging resource export volumes.

Second, central banks have signalled easier monetary policy for longer post-Brexit which is likely to ensure that liquidity conditions remain favourable for growth assets.

Third, while the shift to the left by median voters in Anglo countries resulting in more populist policies is likely to harm long term growth potential, it could actually boost growth in the short term (including under Trump in the US) as it sees a relaxation of fiscal austerity.

Fourth, we may have seen the worst of the commodity bear market. After huge 50% plus falls some commodity markets are moving towards greater balance (notably oil and some metals).

Fifth, deflation risks look to be receding. Oil prices which played a huge role in driving deflation fears look to be trying to bottom and a shift towards more inflationary policies by governments and some central banks are likely to start shifting the risks towards inflation on a 2-5 year view.

Sixth, the profit slump may be close to over. US profits are showing signs of bottoming helped by a stabilisation in the $US and the oil price. Australian profits are likely to rise modestly in the year ahead as the commodity price driven plunge in resource profits runs its course.

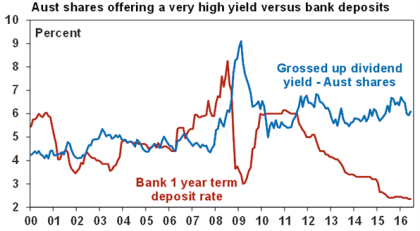

Seventh, the latest falls in interest rates and bond yields have further improved the relative attractiveness of shares and may unleash yet another extension of the search for yield.

Eighth, investors have been more relaxed about the latest decline in the Chinese Renminbi – reflecting slowing capital outflows from China, reassurance from Chinese officials and a growing relaxation about fluctuations in the value of the RMB.

Finally, all the talk has been bearish lately – Brexit, Chinese debt, US slowing, messy Australian election – which provides an ideal springboard for better investment returns!

What about the return outlook?

The August–October period can often be rough for shares. But looking through short term uncertainties and given the considerations in the previous section, – it’s hard to see the outlook for investment markets differing radically from what we have seen over the last few years albeit stronger than over the last 12 months for shares. Growth is not flash but okay, inflation is low and monetary conditions overall are set to remain easy. For the main asset classes, this has the following implications:

-

Cash and term deposit returns to remain poor at around 2%. Investors remain under pressure to decide what they really want: if its capital stability then stick with cash; if its a decent stable income flow then consider the alternatives.

Source: RBA, AMP Capital

-

Ultra-low sovereign bond yields of around 2% or less, with a third of the global bond index in negative yield territory, indicate that the return potential from bonds is low.

-

Corporate debt should provide okay returns. A drift higher in bond yields is a mild drag but with continued modest global growth the risk of default should remain low.

-

Unlisted commercial property and infrastructure are likely to benefit from the ongoing “search for yield”.

-

Residential property returns are likely to be mixed with some cities continuing to see price falls and a further slowing in Sydney and Melbourne property prices. Very low rental yields are not good, particularly in oversupplied apartments.

-

The rising trend in shares is likely to continue as: shares are okay value, monetary conditions remain very easy and continuing moderate economic growth should help profits. Within shares, we favour European, Japanese and Chinese/Asian shares over US shares.

-

Finally, the downtrend in the $A is likely to resume enhancing the case for global shares (unhedged).

Things to keep an eye on

The key things to keep an eye on over the year ahead are:

-

Global business condition PMIs – these currently point to constrained but okay growth.

-

Signs of European countries seeking to leave the Eurozone and investors demanding higher borrowing rates to lend to countries like Italy, seen to be at risk of leaving. Italian banks are also a risk worth keeping an eye on.

-

When/if the Fed starts to raise rates again later this year and the impact on the US dollar.

-

Chinese economic growth readings.

-

Whether Australian non-mining activity keeps improving.

Concluding comments

The September quarter is historically a rough one for shares and the prospect of a Trump victory in the US and worries about Italian banks may cause some nervousness. But looking beyond near-term uncertainties, the mix of reasonable share valuations, continued albeit constrained global growth, easy monetary conditions and a lack of investor euphoria suggest returns are likely to improve from those seen over the last year.

Source: AMP Capital

About the Author

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.