With rate cuts buoying the banking environment, it’s important to keep an eye on where asset quality can move from here. In this article, we assess the value of Australia’s four largest banks, namely Commonwealth Bank, Westpac Banking Corporation, Australia and New Zealand Banking Group (ANZ) and the National Australia Bank (NAB).

Market fundamentals: Earnings growth moderates

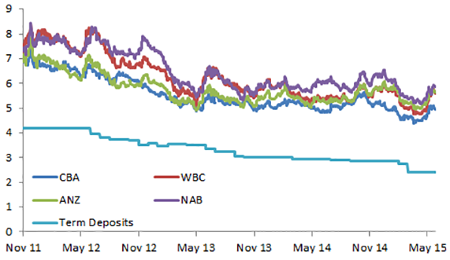

The ‘big four’ banks have impeccable fundamentals right now. However, with investing, it’s not where we are now but where these fundamentals are going that will help determine the price. The banks have increased home loans and improved asset quality since the start of the rate-cut cycle in November 2011. Margin pressure has stabilised as cheaper wholesale funding helps offset declining asset yields along with the benefits of cost and bad and doubtful debts. While the banks’ dividend streams may appeal to investors, they may face capital pressure from tier one capital requirements. With the Reserve Bank of Australia’s rate cuts continuing to buoy the banking environment, it will be important to keep an eye on where asset quality can move from here.

Chart 1 – Dividends are still attractive, but profits to slow

Source: AMP Capital and Bloomberg

Valuations are currently high but should revert

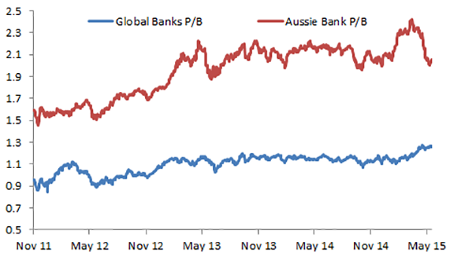

Valuations are now moving to reflect a lower growth profile for earnings and dividends. In saying this, Australia’s major banks still sit on high valuations relative to comparable global peers – see chart 2.

Chart 2: Valuations are probably too high relative to global peers

Source: AMP Capital and Bloomberg

This has been justified as Australia has been a standout economy post-Global Financial Crisis. As the Atlantic recovery builds, we expect that this gap will close. This is happening progressively as our banks de-rate, due to lower profit growth, and offshore banks continue to recover from what was a calamitous cycle for many in this industry overseas. Australia’s ‘big four’ banks yield an average 5.6% in dividends currently and undoubtedly their ability to grow those dividends has pushed their prices higher. That yield spread may have helped the banks outperform the S&P/ASX 200 index by about 20% during the current rate cut cycle.

Final thoughts

The banks will continue to provide strong dividend streams but growth of these dividends will be much harder from here and sustainability of these dividend levels may even prove difficult should earnings dip or capital requirements grow.

|

About the Author Dermot Ryan is Portfolio Manager – Direct Equities, Multi-asset group. Dermot manages concentrated portfolios of Australian equities for AMP’s retail investor base. These portfolios are managed with a longer term outlook and in a tax-effective manner. These portfolios are set along style lines: Income, Growth, Mid-cap and Ethical and hold a maximum of 25 stocks. |