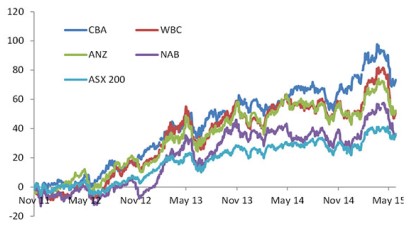

Banks have been top performers before correcting

The banks represent a large portion of Australia’s share market. The ’big four’ banks have been top global performers (in local currency terms) and a very large driver of our stock market rally particularly since the Euro-crisis days of 2012.  All four major banks have outperformed the index. For the past three years rates have been falling and are now at all-time lows, so the banks were able to grow their mortgage books at the same time as problem loans dissipated due in part to these lower rates. As a result, the profits of the ’big four’ have doubled from 2008 levels. This has led to a sustained, steady rise in stock prices, bank profits and a growing stream of dividends.

All four major banks have outperformed the index. For the past three years rates have been falling and are now at all-time lows, so the banks were able to grow their mortgage books at the same time as problem loans dissipated due in part to these lower rates. As a result, the profits of the ’big four’ have doubled from 2008 levels. This has led to a sustained, steady rise in stock prices, bank profits and a growing stream of dividends.

Since their recent reporting season, all our major banks have run into a volatile patch with the sector giving back much of its year-to-date gains. The market has been underwhelmed by the financial results delivered by the banks in May and now in August. With all of the banks increasing their capital by issuing shares the dilution could signal the end of their record profits and dividends.

Why have they given back gains?

Many of the drivers of that growth in profitability and earnings are now slowing and this will lead to some contraction in valuations.

One driver has been cost reduction. Banks have kept a keen eye on costs over this period by capping the growth in employees and implementing productivity and cost-out initiatives. This has led to what the banks call ’positive jaws’, which basically means an increase in profit margins. But cost pressures are re-asserting themselves, meaning this area of margin expansion may be more difficult to achieve going forward.

Another big driver of profits has been the release of balance sheet provisions for bad and doubtful debts. These are reserves the banks hold against loans that are in arrears or at risk of impairment. As interest rates plummeted to all-time lows, these problem loans started to improve to such an extent that the banks are obliged by accounting standards to release those reserves to profits. But with the provisioning for these loans now below pre-GFC levels, they represent a one-off profit driver which may reverse if the cycle weakens. So while profits should still grow this year, some of the factors that were driving these profits are starting to run their course. In the recent reports and updates in August we have seen some slight tick up in provisions, which implies that this trend is unlikely to contribute to profits going forward and may impair growth if the economy softens.

Bank shares have given back some of their large gains

Source: AMP Capital and Bloomberg

Final thoughts

While profits are at all-time highs, earnings growth is slowing and with high starting valuations the banks may come under pressure. Together with industry regulation to increase capital and reduce lending within the investment mortgage market, a more subdued outlook for bank profits is expected along with more challenging times ahead for shareholders as returns on equity moderate.

As banks make up a large part of the Australian share index, most investors will hold these stocks. While banks have recently given back some of their gains made over the past year, they still provide attractive dividends which are an important feature in a yield-starved world.

Source: AMP Capital

About the Author

Dermot Ryan is Portfolio Manager – Direct Equities, Multi-asset group. Dermot manages concentrated portfolios of Australian equities for AMP’s retail investor base. These portfolios are managed with a longer term outlook and in a tax-effective manner. These portfolios are set along style lines: Income, Growth, Mid-cap and Ethical and hold a maximum of 25 stocks.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.