Dermot Ryan, Portfolio Manager, Australian Equites, AMP Capital

Resource companies are enjoying a resurgence in profits based on higher commodity prices and lower unit costs.

Now many of you might think, “well we’ve had booms before.” The big difference this time is that there is still a strong focus on reducing the price of production, even as prices for raw commodities continues to increase.

In the mining boom pre-Global Financial Crisis (GFC) we saw a sharp run up in commodity prices, and companies scrambling over one another to get mines built as quick as possible – irrespective of costs. This led to greenfield expansion and large amounts of money being spent on labour, machinery and procurement and many of these didn’t get a good cost outcome.

Now, I think we are in one of the best periods for franked returns in the mining industry since the that last boom.

It is refreshing to see, in so many cases, mining companies returning money to investors through dividends and buybacks, rather than just being on a mad rush for growth.

Economic Growth

Global economic growth is running hot. In the US, business confidence and employment growth have been rising, and in much of Europe the recovery is underway.

From China, the world’s biggest commodities consumer, we are seeing a lot of demand for seaborne high-grade commodities, and they are also looking to improve their air quality and the environment, which means there may well be a substitution of lower grade Chinese raw materials for higher grade imports.

I think there are interesting opportunities across areas such as energy, iron ore, copper, and also specifically commodities related to electric vehicles. Lithium producers are the biggest winners from this, and there is also strong demand for cobalt and graphite.

As we go through this point in the cycle where demand is still high and interest rates haven’t yet risen there is an opportunity for companies that have de-geared their balance sheets to use some of that capital to invest back into their mines.

Mining expansion rarely comes cheap and the Reserve Bank of Australia has kept interest rates on hold for 21 months now. AMP Capital does not expect a rate rise until 2020. However, should the US Federal reserve raise rates quickly there could be risks for commodity prices and Asia demand.

Mining stock values

Valuations are still quite reasonable in the mining space as well because people want to see how sustainable commodity prices are at this level. It wasn’t that long ago after all, that larger companies found themselves too heavily in debt and struggling to refinance during the GFC.

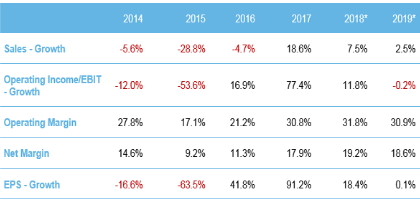

Revenue & Earnings for the Australian Metals and Mining industry group

* Forecast estimates only for 2018 and 2019. Actual future results could differ materially from any forecasts, estimates, or opinions.

Source: Factset Industry Consensus Estimates

The winners are those who can add incremental production to existing plants and reduce their unit costs per commodity and come down the cost curve. This particularly favors companies with expandable tier one assets.

Now, we seem to be in a more considered period where most moving factors point towards better returns at any given commodity prices. This is really encouraging for Australian investors.

Companies too are much more focused on capital allocation and returning cash to shareholders. These periods of high dividends in deeply cyclical sectors like mining don’t last forever but can be enjoyed by investors in the current market.

Source: AMP Capital 13 June 2018

Author: Dermot Ryan, Portfolio Manager, Australian Equites, AMP Capital

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.