It seems there is constant hand wringing about the risks around the Chinese economy with the common concerns being around unbalanced growth, debt, the property market, the exchange rate and capital flows and a “hard landing”. This angst is understandable to some degree. Rapid growth as China has seen brings questions about its sustainability. And China is now the world’s second largest economy, its biggest contributor to growth and Australia’s biggest export market so what happens in China has big ramifications globally. But despite all the worries it keeps on keeping on and recently growth has been relatively stable. This note looks at China’s growth outlook, the main risks and what it means for investors and Australia.

Stable growth, benign inflation

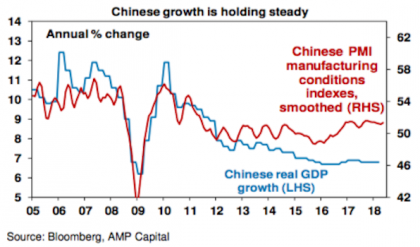

Chinese growth slowed through the first half of this decade culminating in a growth and currency scare in 2015 which saw Chinese policy swing from mild tightening towards stimulus. This has seen pretty stable growth since 2016 of around 6.8% year on year. Consistent with this, business conditions PMIs have also been stable (see the next chart) and uncertainty around the Renminbi has fallen & capital outflows have slowed.

Source: Bloomberg, AMP Capital

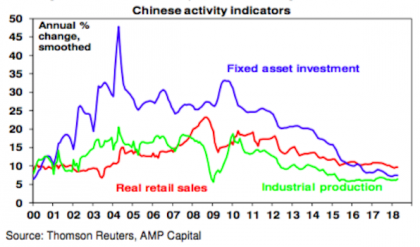

April data saw industrial production and profits accelerate but investment and retail sales slow a bit. Electricity consumption, railway freight and excavator sales have lost momentum from their highs. But the overall impression is that growth is still solid.

Source: Bloomberg, AMP Capital

While there is a need for China to rebalance its growth away from investing for exports, the slowdown in investment growth to below that for retail sales, imports growing faster than exports and the shrinkage in China’s current account deficit from 10% of GDP to 1% of GDP suggests this occurring.

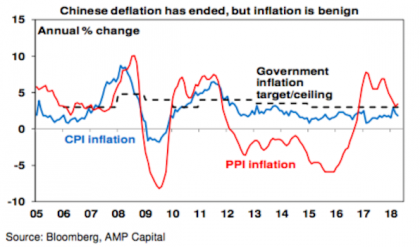

Meanwhile, inflation in China is benign with producer price inflation around 3% and consumer price inflation around 2%.

Source: Domain, AMP Capital

Policy neutral

Chinese economic policy has been relatively stable recently. There has been some talk of boosting domestic demand and bank required reserve ratios have been cut. But the latter appears to have been to allow banks to repay medium term loan facilities, interest rates have been stable and growth in public spending has been steady at 7-8% year on year.

Growth and inflation outlook

We expect Chinese growth this year to slow a bit as investment slows further to around 6.5% and consumer inflation of 2-3%.

Key risks facing China

There are four key risks facing China. First, the policy focus could shift from maintaining solid growth to speeding up medium-term economic reforms and deleveraging (or cutting debt ratios) that could threaten short-term economic growth. Some expected this to occur after the 19th National Congress of the Communist Party was out of the way late last year. And the removal of term limits on President Xi Jinping could arguably make him less sensitive to a short-term economic downturn. However, so far there is no sign of this and the authorities seem focused on maintaining solid growth.

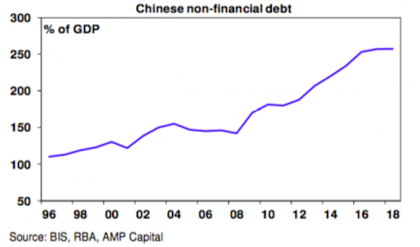

Second, China’s rapid debt growth could turn sour. Since the Global Financial Crisis, China’s ratio of non-financial debt to GDP has increased from around 150% to around 260%, which is a faster rise than has occurred in all other major countries.

Source: RBA, AMP Capital

This has been concentrated in corporate debt and to a lesser degree household debt and has been made easier by financial liberalisation and a lot of the growth has been outside the more regulated banking system in “shadow banking”. An obvious concern is that when debt growth is rapid it results in a lot of lending that should not have happened that eventually goes bad. However, China’s debt problems are different to most countries. First, as the world’s biggest creditor nation China has borrowed from itself – so there’s no foreigners to cause a foreign exchange crisis. Second, much of the rise in debt owes to corporate debt that’s partly connected to fiscal policy and so the odds of government bailout are high. Finally, the key driver of the rise in debt in China is that it saves around 46% of GDP and much of this is recycled through the banks where it’s called debt. So unlike other countries with debt problems China needs to save less and consume more and it needs to transform more of its saving into equity rather than debt. Chinese authorities have long been aware of the issue and growth in shadow banking and overall debt has slowed but slamming on the debt brakes without seeing stronger consumption makes no sense.

Third, the risk of a trade war has escalated with Trump threatening tariffs on $50-150bn of imports from China and restrictions on Chinese investment in the US and China threatening to reciprocate. While “constructive” negotiations have commenced and have seen China commit to buying more from the US & to strengthen laws protecting intellectual property which saw the US initially defer the tariffs and restrictions, Trump has indicated that they will be implemented this month which looks to be aimed at prodding China to move rapidly (and appeasing his base). Ultimately, we expect a negotiated solution, but the risks are high and a full-blown trade war with the US could knock 0.5% or so off Chinese short-term growth.

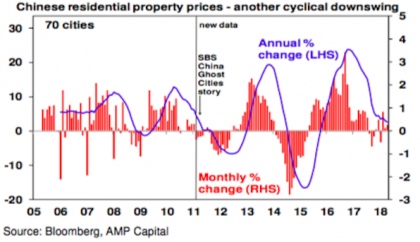

Finally, with the Chinese residential property market slowing again there is naturally the risk that this could turn into a slump. It’s worth keeping an eye on but absent an external shock looks doubtful. The “ghost cities” paranoia of a few years ago – it first aired on SBS TV way back in 2011 – has clearly not come to much. It’s doubtful China ever really had a generalised housing bubble: household debt is low by advanced country standards; house prices haven’t kept up with incomes; and while there’s been some excessive supply, this is not so in first tier cities; and the quality of the housing stock is low necessitating replacement. So, I think the property crash fears continue to be exaggerated and the latest bout of weakness in prices looks to be just another cyclical downswing in China of which there have been several over the last decade.

Our assessment remains that these risks are manageable, albeit the trade war risk is the hardest for China to manage given the erratic actions of President Trump. The Chinese Government has plenty of firepower to support growth though, so a “hard landing” for Chinese growth remains unlikely for now.

The Chinese share market

Since its low in January 2016 the Chinese share market has had a good recovery. But Chinese shares are trading on a price to earnings ratio of 12.8 times which is far from excessive.

With valuations okay and growth continuing, Chinese shares should provide reasonable returns, albeit they can be volatile.

Implications for Australia – not yet 2003, but still good

Solid growth in China should help keep commodity prices, Australia’s terms of trade and export volume growth reasonably solid. This, along with rising non-mining investment and strong public investment in infrastructure, will offset slowing housing investment and uncertainty over the outlook for consumer spending and will keep Australian economic growth going. However, with strong resources supply (and still falling mining investment) we are a long way from the boom time conditions of last decade and growth is likely to average around 2.5-3%. Rising US interest rates against flat Australian rates suggests more downside for the $A, but solid commodity prices should provide a floor for the $A in the high $US0.60s.

Key implications for investors

-

Chinese shares remain reasonably good value from a long- term perspective, but beware their short-term volatility.

-

Solid Chinese growth should support commodity prices and resources shares

Source: AMP Capital 04 June 2018

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.