There is even talk of lenders managing their exposure by focussing on postcodes. This is all in response to increasing pressure from the banking regulator APRA (the Australian Prudential Regulation Authority) demanding that the 10% cap on property investor lending growth that it announced last December be adhered to.

Those who have been around for a while might wonder what is going on. Isn’t this what used to happen in the dim dark days before the enlightenment of financial de-regulation in the 1980s? The answer is yes and the term “macro prudential regulation” – in reference to using prudential controls on lending to influence the economic cycle – is just a fancy term for what went on in the past.

So why has it made a comeback?

The focus on varying prudential controls to achieve macro-economic outcomes was quite common up until the early 1980s but went the way of the dodo when it was concluded that it was only leading to distortions in the financial system, as people found a way around them. So while financial system regulators, like APRA, continued to ensure that prudential standards were met, from the mid 1980s varying interest rates to control the housing and economic cycle became the norm. And this worked reasonably well.

The last major boom in Australian property prices ended around 2004. This was a cracker and saw: average home prices around Australia rise an average of nearly 15% per annum over the five years to the end of 2003; a massive surge in housing related credit with property lending growing 21% and property investor lending growing 30% in 2003; this in part was fuelled by property spruikers running property investment seminars on a grand scale; and there was little doubt that house price gains were being extrapolated off into the future in investors’ minds and that this in turn was driving more property investment.

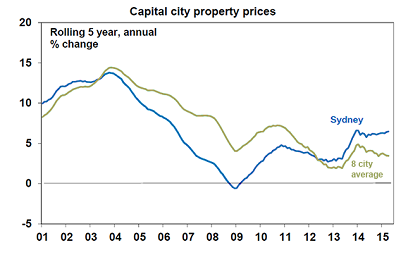

Source: CoreLogic RP Data, AMP Capital

The surge into 2003 took the property price to household income ratio from around three times to around five to six times and saw real property prices go from well below trend to well above.

As a result concern about a property bubble and poor housing affordability came to the fore. It was “cooled down”, not by prudential controls but by a combination of “jawboning” by then RBA Governor Ian Macfarlane warning against the dangers of property speculation and then the start of an interest rate tightening cycle as the economy improved. The collapse of a high profile property spruiker’s business and poor housing affordability also helped.

But while the prudential regulator made sure that lending standards were being maintained, prudential controls were not varied to achieve macro-economic outcomes.

This time is a bit different for several reasons.

-

First, property price gains are nowhere near as strong – over the last five years average capital city home prices have risen at just 3.5% pa. For Sydney it’s just 6.5% pa.

-

Second, the gains are not broad based – while Sydney home prices are up 14.5% over the year to April, for the other capital cities the gain is just 1.7%.

-

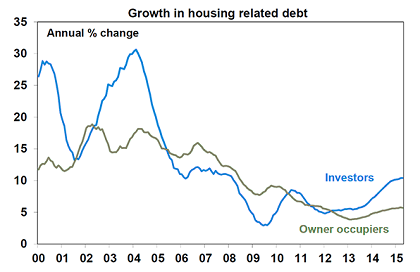

Third, credit growth is running at a fraction of what was seen in 2003 with total housing related credit up 7.2% over the year to April and investor credit up 10.4%.

Source: RBA, AMP Capital

-

Finally, unlike in 2003 and 2004 the economy is much weaker. Back then growth had been picking up after a soft patch and was being helped by a super low $A, households happy to take on more debt – remember the line about households having an ATM in their living room – and the start of the mining boom. Now the economy has been sub-par for several years as the mining boom is unwinding. In fact, the rest of the economy needs very low interest rates.

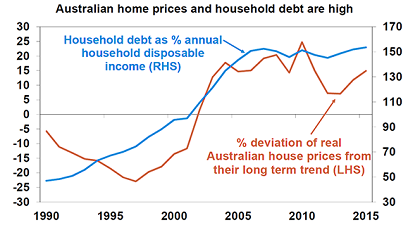

But of course it is never that simple as the RBA and regulators are aware that expressed relative to household income both home prices and household debt levels are already very high as is the ratio of house prices compared to their long term trend – having never really unwound from the surge into 2003-04. See the next chart. And so they are fearful of letting low interest rates drive home prices much higher given the risk to the financial system and economy should they then fall sharply.

Source: RBA, ABS, AMP Capital

So to balance all these cross currents there has been a return to using macro prudential controls in order to allow the low interest rates that the economy as a whole needs but at the same time to keep a lid on the property market.

Will it work?

Only time will tell on this one. APRA is pretty adamant that it wants to see growth in property investment lending slow into the second half of the year and if lenders don’t tow the line then tougher action is likely. So my feeling is that it probably will work and we should expect to see a slowing in the availability of credit for property investors and as a result some slowing in home price growth in Sydney (maybe back to around 8% pa) and to a lesser degree Melbourne over the next year. However, a downturn in property prices will likely have to await the start of interest rate hikes and that’s unlikely until 2017.

However, there are several risks around this. APRA’s 10% “cap” on property investor lending growth could prove too lax and on the other side it’s hard to know when such regulatory tightening has gone too far in which case the property market could slow more than expected. There is also a danger that it hits cities that are weak anyway (basically all the capital cities except Sydney and Melbourne). And longer term, lenders and borrowers may try to find a way around such prudential controls.

But hopefully by then the economy will have returned to normal and we can go back to relying on interest rates to control the property cycle.

In the meantime, the use of macro prudential controls helps provide the RBA with flexibility to keep interest rates down and if necessary to cut them again if needed. In fact, after the latest figures on the business investment outlook another interest rate cut is now looking increasingly likely.

About the Author

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.