The US election – populists versus the establishment

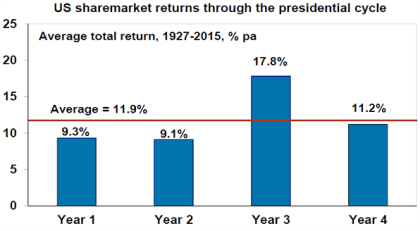

First some facts. The election year, or Year 4 in the 4-year US presidential cycle, is normally an ok year for US shares. However, when it is in the eighth year of a presidency it has been poor with an average loss of -3.4% since 1927, albeit this is pushed down by the -37% outcome due to the GFC in 2008.

Source: Bloomberg, AMP Capital

Historically, US shares have actually done better under Democrat presidents with an average return of 15.4% pa since 1945 compared to an average return over the same period under Republican presidents of 10.5% pa.

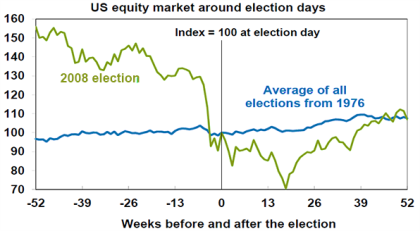

US elections themselves show little sign of having a major impact on share markets. See the next slide, which shows the US share market performance from a year before till a year after all presidential elections since 1976. Of course, the share market around the 2008 election was dominated by the GFC.

Source: Thomson Financial, AMP Capital

This election is looming as significant for markets given the success of populist candidates – notably Donald Trump on the Republican side and to a lesser degree Bernie Sanders in the Democrats – which raises the risk of a less business and less market-friendly president. Bernie Sanders is left wing and he and Trump tend to be anti-free trade and tough on banks/Wall Street. A populist Republican like Ted Cruz may also be less inclined to intervene to support the economy in the event of a crisis. Against this, even if a populist does get up as president, the centrist or status quo dominance of the broad rump of Republicans and Democrats in Congress (with Republicans likely controlling both houses) should limit the power of the president to enact extreme or less market friendly policies. More importantly, it’s not clear the populists will get up anyway. Hillary Clinton appears to be beating Sanders. Meanwhile, Trump is winning but his vote appears stuck around 30-45%, meaning that most Republicans are voting for other candidates. As the Republican field narrows, it’s likely that the GOP establishment will swing in behind the last remaining candidate (likely to be Marco Rubio). Time will tell. March 1 or Super Tuesday is the next big day to watch in the primaries, but it’s likely that the contest in November will be between two establishment candidates (Clinton v Rubio?) who by then will have migrated to the centre of US politics in order to win with nowhere near the policy differences that are currently getting an airing. In time, a Clinton presidency is likely to drift to the centre given the reality of US politics with Republican control of Congress (just like Bill Clinton did in the 1990s) so a market unfriendly outcome is unlikely. There could be a few scares along the way though.

Brexit – should we stay or should we go?

Following the European Union agreement on the “special status” of the UK in Europe, the date for the Brexit referendum has been set as June 23rd. A vote to leave would be seen as a big negative for the UK given the threat it would pose to its access to EU markets, its financial sector and labour mobility. The size of this impact would depend on what sort of exit is negotiated with the EU but has been variously estimated at somewhere between -0.6% and -2.8% of UK GDP, which would also adversely affect UK assets (which explains sterling’s recent fall). However, Britain is not in the Eurozone currency union so a Brexit would not pose the existential threat to it that, say, a Grexit has in recent times. However, the real risk would be if a Brexit emboldened support for Marine Le Pen in France and a push towards a Frexit (French exit). This would seriously threaten the EU and the Eurozone (as France is a member of both). It seems unlikely though given the role of France and Germany at the core of the European Union and the Eurozone currency union. Polls suggest a Brexit is too close to call although I lean towards a stay vote.

Populism in Europe

The Eurozone is riven with political issues that occasionally flare up and cause market scares on fears that they might trigger a break-up of the Euro. High unemployment post the sovereign debt crisis is a key driver of increased support for populist parties & it’s been pushed along by the migration crisis.

-

Spain is likely headed towards another election after the unclear result from its December election and the push for independence from Catalonia is yet to be resolved. However, Spain is not Greece. First, 65% of the electorate voted for pro-Euro parties in the December election so a Spexit (Spanish exit from the Euro) is not on the agenda. Second, left wing Podemos got only 21% of the vote leaving it a long way from being able to govern in contrast to Syriza in Greece. Unlike in Greece, much of the heavy lifting on reforms has already been done in Spain. Finally, the Catalonian issue could drag on for a while as a majority of Catalans don’t appear to support independence and constitutional issues will make a move out of Spain difficult.

-

Greece is likely to continue to see occasional flare-ups with the Government only having a small minority in parliament. So we may not have heard the last of Grexit. Then again, staying in the Euro still has majority support in Greece.

-

More broadly, the European migration crisis has seen a rise in support for populist anti-establishment parties. This could subside though given a harder line on immigration from centrist leaders like Angela Merkel.

None of these issues are likely to pose a serious threat to the Euro but the risk will remain if European economic growth slows again and unemployment rises again, triggering a further rise in support for populist parties. As such they are worth watching.

Iran v Saudi Arabia, IS versus them all

The Middle East has long been an area of tension and conflict. In recent times the dynamics have changed as the US has “pivoted” to Asia and trade bans on Iran have been eased or removed. As a result, a long-time tension between Sunni Saudi Arabia and Shia Iran has come to the fore. The defeat of IS could worsen this tension as it will further entrench Iran’s influence on Iraq along Saudi Arabia’s border. This in large part explains why OPEC has fallen apart as Saudi Arabia has sought to maintain its market share versus its Shia rivals of Iran and Iraq. All of which means that Saudi Arabia won’t be cutting back on its oil production anytime soon. At the same time Iran is ramping up its own oil production. None of which is good for the oil price. Against this. though, even though Saudi Arabia has been ramping up its defence spending as the US commitment in the region has declined, direct conflict between Saudi Arabia and Iran still looks unlikely.

Meanwhile the terror threat from IS remains and could intensify if it looks like being defeated in Iraq and Syria. Then again, the world has become used to this with the impact on financial markets of terrorist attacks since 9/11 seemingly declining.

South China Sea

Tension over disputed islands in the South China Sea involving China have been brewing for years. At its core, China feels a bit blocked in by the geography of the South China Sea and, as a rising geopolitical power, is seeking to flex its muscles and take a stand on the issue. Of course, this falls foul of its neighbours who also have claims on the islands and the declining geopolitical power, the US, which would prefer to contain China and of course guarantee sea traffic through the disputed area. Hopefully, common sense prevails but the risk of an escalation or occasional flare-up in this dispute is clearly there.

Australian election

Compared to all these issues, the Australian Federal election – which is due to be held later this year, but could come earlier – is likely to be relatively tame. So far, not enough has been released in terms of the campaign policies of the major parties. Perhaps the big disappointment in the last few weeks is that the debate around tax reform seems to have degenerated yet again into tit for tat scare mongering rather than focussing on visionary fundamental reform. However, two things are worth noting. First, Labor seems more focussed on addressing the budget deficit by looking for pots of money to raise revenue from (such as via curtailing access to negative gearing and the capital gains tax discount), whereas the Coalition still looks to be more focussed on containing government spending and using any wind back in tax concessions to cut income tax. Second, changes to Senate voting procedures (that will have the effect of cutting back on minor party representation) could have the effect of making the Senate and hence the business of government in Australia far more effective. In other words, Australia is one country where the populist influence could end up being substantially curtailed.

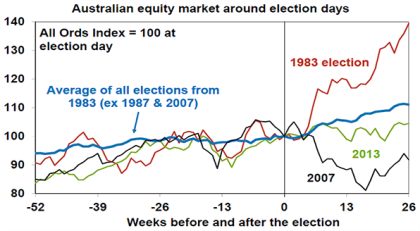

Historically, Australian shares have performed better under Coalition governments (with an average return of 12.7% pa since 1945) than under Labor (with an average 10.7% pa). During the last 30 years, Australian shares have generally risen after Federal elections. This is evident in the next chart, which shows Australian share prices from one year before till six months after Federal elections since 1983. This is shown as an average for all elections (but excludes the 1987 and 2007 elections given the 1987 global share crash and the start of the global financial crisis in 2007). What is clear is that after elections shares tend to rise more often than they fall.

Source: Thomson Financial, AMP Capital

Implication for investors

Politics is looming large as an issue for investors this year. The bulk of the issues identified here should ultimately turn out okay for investors, but it’s worth keeping a close eye on them.

AMP Capital Markets 25th February 2016

About the Author

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.