The 2018-19 Budget will be the last before the next election (due by May 2019) and so had to provide pre-election goodies but in a way that keeps the return to surplus on track. Thanks to an improvement in the budget position since the Mid-Year review, of around $7bn per annum, this has been made relatively easy. A modest fiscal stimulus will help households, but the main risk is that the revenue boost proves temporary.

Key Budget Measures

As always, most of the measures in the Budget were pre-announced or leaked. The goodies include:

-

Income tax cuts from July for low to middle income earners of up to $10 a week which is mainly achieved by lifting the Low Income Tax Offset and raising the $87,000 tax threshold to $90,000.

-

A plan for broader tax cuts starting in 2022, which from 2024 includes removing the 37% tax bracket and having the 32.5% tax bracket go all the way up to $200,000.

-

Dropping the planned 0.5% Medicare levy increase.

-

Ongoing commitment to cut the corporate tax rate to 25% for large companies by 2026-27.

-

Extension of the small business instant asset write off.

-

Increased spending on home aged care, various concessions for older Australians related to superannuation contributions and work tests, more hospital funding and new products listed on the Pharmaceutical Benefits Scheme.

-

An extra $25bn in infrastructure spending including the Melbourne rail link, Bruce Highway, Gold Coast/Brisbane M1, road and rail in WA and North-South Corridor in SA.

This is only partly offset by various savings including an illicit tobacco tax and the usual tax integrity measures to target the black economy and multinational tax avoidance.

Stronger revenue, but tax cuts

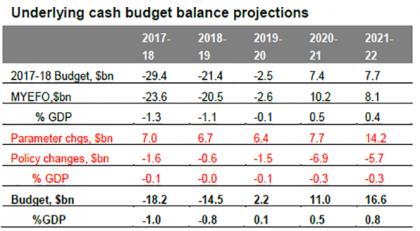

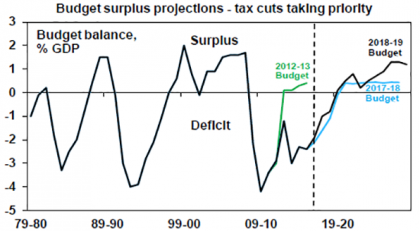

Thanks to stronger corporate revenue (due to reduced tax losses and higher commodity prices), stronger personal tax revenue thanks to higher employment and reduced spending the 2017-18 budget deficit is projected to come in at $18.2bn compared to $23.6bn in the Mid-Year review. The Government has assumed that much of this revenue boost will continue (see the “parameter changes” line in the table below) but has only used a bit of it to fund tax cuts and other measures. The net result is that the budget is projected to continue to track to a surplus – which is now expected to be reached one year earlier in 2019-20 albeit its only wafer thin at $2.2bn or 0.1% of GDP. The move back to surplus is slowed slightly by the fiscal easing from policy changes (predominately tax cuts). For example the 2018-19 deficit is projected to fall to $14.5bn but it would have fallen to $13.8bn were it not for the fiscal easing. That said the fiscal easing is small at 0.1 to 0.3% of GDP over the next few years and the progressive shift from deficit to surplus will mean that it will take more out of the economy than its putting back in.

Source: Australian Treasury, AMP Capital

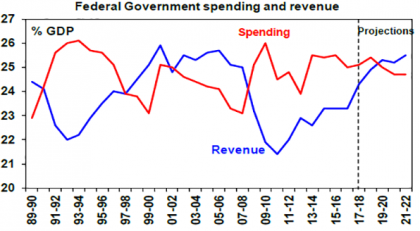

The planned tax cuts for higher income earners next decade are designed to satisfy the Government’s commitment from the 2014 Budget to cap tax revenue at 23.9% of GDP (or total revenue once dividends are allowed for as shown in the chart below at 25.4% of GDP) on the grounds that this is around the historic highs (reached in the Howard resources boom years). This cap is now projected to be reached in 2021-22.

Source: Australian Treasury, AMP Capital

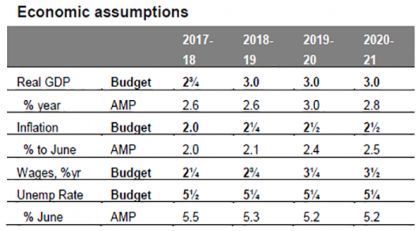

Economic assumptions

Most of the assumptions look reasonable, except that the 3% growth assumption is a bit on the optimistic side and it remains hard to see wages growth rising to 3.5% over the next four years given unemployment is not expected to fall much.

Source: Australian Treasury, AMP Capital

Assessment and risks

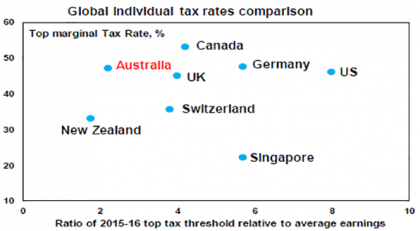

This is an upbeat Budget. First the near-term tax cuts for low to middle income earners will help households at a time of soft wages growth, falling home prices and tightening lending standards. This will be very small though at $10 a week (a sandwich and milkshake!) and will be slightly dampened because the majority of the benefit will come when taxpayers do their 2018-19 tax return sometime after June next year. Second, the Budget recognises that we cannot rely on bracket creep to cut public debt. The Australian tax system is already highly progressive and is becoming more so with the top 10% of earners accounting for 45% of income tax revenue, up from 36% two decades ago. Compared to other comparable countries the top marginal tax rate is both relatively high and kicks in at a relatively low multiple of average earnings. If this is not limited it risks dampening incentive and productivity. Third, the continuing focus on infrastructure is good for short term growth, productivity and “crowding in” private investment. It will help to keep the economy growing.

Source: ATO, AMP Capital

Finally, thanks to much of the revenue surge being saved the budget remains on track to return to surplus, in fact a year earlier than previously projected.

Source: Australian Treasury, AMP Capital

The main risks though are that we still be seeing a record run of 11 years of budget deficits. While our net public debt to GDP ratio is low at 19% compared to 81% in the US, 69% in the Eurozone and 153% in Japan, comparing ourselves to a bad bunch is dangerous and they are all a bit different with Europe and Japan borrowing from themselves and the US benefitting from its reserve currency status. The run of deficits being projected in the Budget still swamps those of the 1980s and 1990s. And this is without the deep recessions of the early 1980s and 1990s! Rather we have achieved this thanks to a combination of ramping up spending on a whole range of things without facing up to how they will be paid for. Unlike prior to the GFC we have nothing put aside for a rainy day (when net public debt was negative) and there is a risk that the revenue surprise seen lately will prove temporary if global growth or employment slows. This may particularly be a risk around 2020 if the global economy starts to slow again in response to Fed tightening.

We continue to rely on assuming strong revenue growth. Of course, bracket creep helps, but even with the tax cut plan the Budget’s projections for average revenue growth of a 5.6% per annum over the next four years seem a little high when nominal growth is forecast to run around 4.5%. The biggest risk remains that wages don’t accelerate as assumed leading to a resumption of poor personal tax collections.

Implications for the RBA

While this Budget should provide some boost to confidence – for which the next two months’ confidence figures should be watched closely, the fiscal boost to the economy and household income is modest with the latter only showing up sometime in second half 2019. So it’s unlikely to be enough to speed the economy up. As such, we see no reason to change our view that the RBA will remain on hold out to 2020.

Implications for Australian assets

Cash and term deposits – with interest rates remaining low, returns from cash and bank term deposits will remain low.

Bonds – a major impact on the bond market from the Budget is unlikely. With Australian five year bond yields at 2.4%, it’s hard to see great returns from bonds over the next few years albeit Australian bonds will likely outperform US/global bonds.

Shares – the potential boost to confidence from this Budget could be a small positive for the Australian share market. But it’s hard to see much impact on shares.

Property – the Budget is unlikely to have much impact on the property market. Interesting to note that the 2017 budget saw an effort to encourage retirees to sell the family home whereas this year there are measures to help them stay in it! We expect Sydney and Melbourne home prices to fall further.

Infrastructure – continuing strong infrastructure spending should in time provide more opportunities for private investors as many of the resultant assets are ultimately privatised.

The $A – the Budget alone won’t have much impact on the $A. With the interest rate differential in favour of Australia continuing to narrow the downtrend in the $A has further to go.

Concluding comments

The 2018-19 Budget has a sensible focus on providing a small boost to households (with the full impact of tax cuts not occurring until next decade) and to infrastructure at the same time as maintaining a return to surplus. The main risks are around whether the recent revenue windfall to the budget proves temporary and the assumptions for continued strong revenue growth.

Source: AMP Capital 9 May 2018

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.