A pick-up in the housing sector was a necessary part of the adjustment in the Australian economy following the end of the mining boom. The RBA started cutting interest rates in 2011, home buyers returned, home prices rose and this has all encouraged a dwelling construction boom that has helped offset the mining investment slump. However, as always the surge in home prices has refocussed attention on whether there is a property bubble and how it might end.

Analysing the Australian residential property market is a bit like Groundhog Day as the big picture fundamental issues don’t really change much in that Australian housing is expensive, affordability is poor, household debt is high and there is a constant debate as to whether there is a crash around the corner. This has been the case ever since 2003.

So quite clearly the issues around the property market are much more complex than many would see them. This note takes a look at where we are now in the Australian residential property cycle and implications for investors.

Overvalued with too much debt…

At a big picture level it’s hard to get away from the view that Australian property is expensive and household debt is high:

-

According to the 2015 Demographia Housing Affordability Survey the median multiple of house prices to household income is 6.4 times in Australia versus 3.6 in the US and 4.7 in the UK.

-

On the basis of the ratio of house prices to rents adjusted for inflation relative to its long term average, Australian houses are 37% overvalued and units 14% overvalued.

-

The ratios of house prices to incomes and rents in Australia are at the high end of OECD countries. By contrast the US is near the low end in the OECD.

-

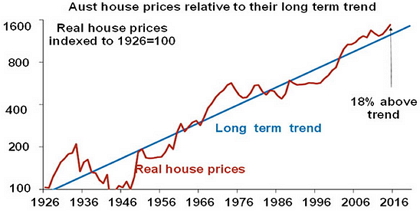

Real house prices have been running above trend since 2003. While the excess above trend eased from 2010 it has blown out again in the last two years.

Source: ABS, AMP Capital

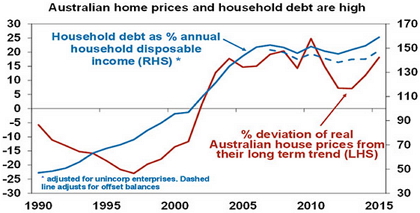

The shift to overvaluation has come higher household debt. The next chart shows the deviation in house prices from their long term trend against the ratio of household debt to income.

Source: ABS, RBA, AMP Capital

Naturally all of this has led to concern that Australia is in a housing bubble that will inevitably burst.

…but not as simple as it looks

However, it’s not as simple as this:

-

First, the big surge in home prices and household debt actually took place from the late 1990s into early last decade. Since then measures of overvaluation and the debt to income ratio haven’t changed much (esp after allowing for mortgage offset accounts). See the last chart. In other words the surge in home prices and debt was unrelated to the mining boom, except in some cities like Perth.

-

Second, the claims around negative gearing, foreign and SMSF buying driving the problem don’t really stack up: negative gearing has been around for a long time and while foreign and SMSF buying has played a role it looks to be small and foreign buying is concentrated in certain areas.

-

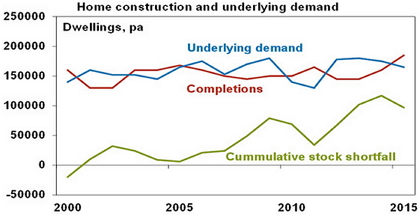

Third, a more fundamental factor explaining the persistence of “overvalued” home prices in Australia relative to other countries is constrained supply. Australia has had a chronic undersupply which has been worsening until recently. This can be seen in the next chart which tracks housing starts versus underlying demand. The cumulative undersupply on this measure reached above 100,000 dwellings last year. The main reason behind the slow supply response appears to be tough land use regulations in Australia.

Source: ABS, AMP Capital

-

Fourth, while household debt has gone up a lot there has not been anything like the deterioration in lending standards seen in other countries. Much of the increase in debt has gone to older, wealthier Australians. Bad debts and arrears remain low. While loan size has increased, Australians’ seem focussed on cutting their debt once they get it.

-

Finally, while Sydney and Melbourne have had all the characteristics of a bubble of late (overvaluation, rapid price gains, a desire to get in for fear of missing out), the rest of Australia has not. So it’s dangerous to generalise.

Source: CoreLogic, RP Data, AMP Capital

Despite all these qualifications, high house prices combined with high household debt to income ratios suggest Australia is vulnerable should something threaten the ability of households to service their mortgages. As such the RBA and APRA have been right to try and slow the property market down

So where are we now?

Our assessment is that the national property market is cooling.

-

APRA’s measures to slow lending to property investors are clearly biting with lending to investors slowing.

-

The Westpac-MI consumer sentiment survey shows a sharp fall in consumers’ assessment as to whether now is a good time to buy a dwelling, led by NSW.

-

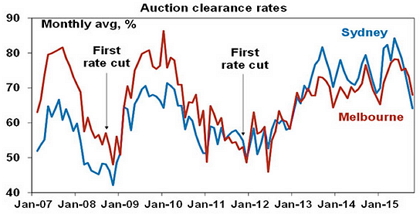

Auction clearance rates have slowed.

Source: Australian Property Monitors, AMP Capital

However, this slowdown is likely to be concentrated in Sydney & Melbourne, which are likely to see price growth slow to around 5% over the year ahead. Price growth is likely to remain negative in Perth and Darwin as the mining boom continues to unwind. Hobart & Adelaide are likely to see continued moderate property growth, but Brisbane may start to pick up a bit.

Nationwide price falls are unlikely until the RBA starts to raise interest rates and this is unlikely before 2017. And then in the absence of a recession or rapid interest rate hikes price falls are more likely to be 5-10% as was seen in the 2009 and 2011 down cycles than anything worse. In fact, the cooling in investor demand in Sydney and Melbourne are likely to provide greater flexibility for the RBA to cut interest rates again.

What to watch for a harder landing?

I would nominate the following:

-

A recession – much higher unemployment could clearly cause debt servicing problems and hence forced sales. The risk at present looks manageable though at around 20%.

-

A surge in interest rates – but the RBA knows about the increased debt sensitivity of households so this would require the RBA to get it wrong badly.

-

Property oversupply – this is a risk but would require the current construction boom to continue for several years.

Implications for investors

There are several implications for investors:

-

First, over the very long term residential property adjusted for costs has provided a similar return for investors as Australian shares, at around 11-11.5% pa. So there is role for residential property in investors’ portfolios.

-

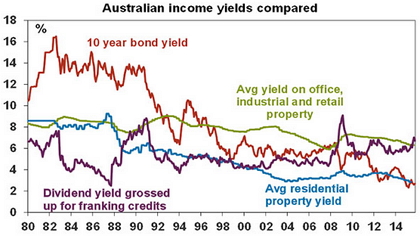

Second, housing is looking somewhat less attractive as a medium term investment. It is now expensive on all metrics and offers very low income (rental) yields compared to all other assets except bank deposits and Government bonds. The gross rental yield on housing is around 2.8% (after costs this is around 1%), compared to yields of 6% on commercial property and 6.7% for Australian shares (with franking credits). This means that a housing investor is more dependent on capital growth to generate a decent return.

Source: Bloomberg, REIA, AMP Capital

-

Third, these comments relate to housing in aggregate. For those who want to look around there are pockets of value, eg in regional areas. You just have to look for them.

-

Finally, investors need to consider their exposure to Australian residential property generally. As a share of total household wealth its nearly 60%. Once allowance is made for indirect property exposure via Australian shares (banks, property trusts, etc) it’s even higher. I am not in the property crash camp but the risk of it does reinforce our assessment that Australian investors should have a decent exposure to say unhedged global shares because it could provide an offset should something go wrong with Australian housing.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.