The period since the Global Financial Crisis (GFC) has seemed unusual in the sense that periodic crises and post GFC caution prevented the global economy from overheating and excesses building, in turn preventing the return of the conventional economic cycle. Many of course concluded this was permanent and that inflation would never rise again (with talk of structural stagnation, the Amazon effect, etc). However, it’s becoming increasingly clear the global economy is moving out of its post GFC funk – with growth picking up and signs that inflation will too (led by the US) – and arguably returning to a more normal investment cycle. The pullback in shares and surge in volatility seen this month likely indicates an adjustment in investor expectations to reflect this. This note looks at what to watch.

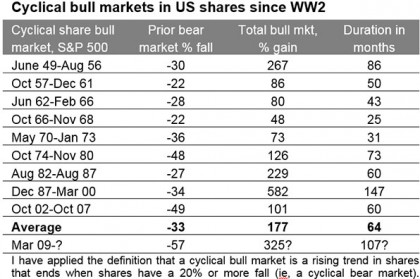

The long and strong US bull market

Source: Bloomberg, AMP Capital.

This makes it the second longest since World War Two and the second strongest in terms of gain. And according to the US National Bureau of Economic Research the current US economic expansion is now 104 months old and compares to an average expansion of 58 months since 1945. This naturally begs the question whether recession is around the corner leaving the US and hence global shares vulnerable to a major bear market?

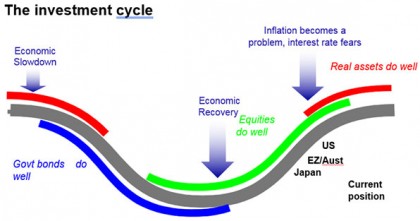

The investment cycle is maturing

Source: AMP Capital

A typical cyclical bull market in shares has three phases: scepticism – when economic conditions are weak and confidence is poor, but smart investors see value in shares helped by ultra-easy monetary conditions; optimism or the “sweet spot” – when profits and growth strengthen and investor scepticism gives way to optimism while monetary policy is still easy; euphoria – when investors become euphoric on strong economic and profit conditions, which pushes shares into clear overvalued territory and excesses appear, forcing central banks to become tight triggering an economic downturn, which combines with overvaluation and investors being fully invested to drive a new bear market.

Typically, the bull phase lasts five years. However, “bull markets do not die of old age but of exhaustion” – their length depends on how quickly recovery proceeds, excess builds up, inflation rises and extremes of overvaluation and investor euphoria appear.

This process has taken longer than normal following the GFC because periodic crises or aftershocks from the GFC – eg, the 2010-2012 Eurozone sovereign debt crisis and the 2015-16 global growth scare both of which were associated with mini bear markets globally and 19% and 14% falls in US shares respectively. This combined with post GFC consumer and business caution have prevented the global economy from overheating and excesses building and share markets going into euphoria, that then sets the scene for the next major bear market.

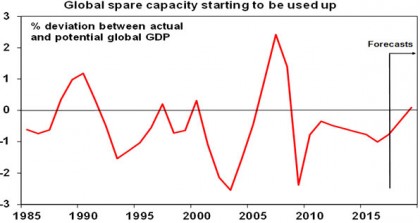

However, this is starting to change. Global growth forecasts have stopped being revised down and are now being revised up. Global growth this year and next will likely be around 3.9% which is above potential. So global spare capacity is starting to be used up.

Source: IMF, AMP Capital

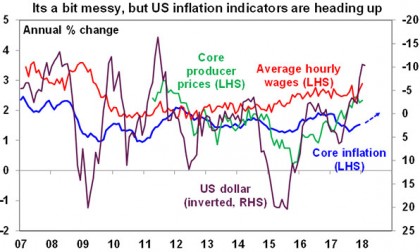

Fiscal austerity has given way to fiscal stimulus – at least in the US (with tax cuts and the removal of spending caps) – which with a lag will further boost growth. Inflationary pressures are building in the US – which is further advanced in the economic cycle than Europe, Australia and Japan (see the first chart) – with a tight labour market, rising wages growth and accelerating import prices (flowing from the falling $US) and producer price inflation.

Source: Bloomberg, AMP Capital

Not at the top yet

-

overall private sector debt growth is modest in most countries (except for corporate debt in the US and China);

-

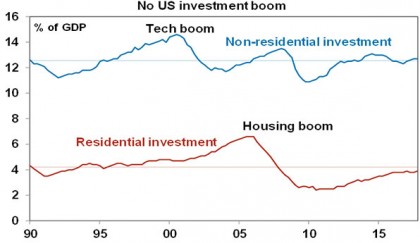

while investment is starting to pick up globally, there is no sign of overinvestment. While the US is further advanced, even here business investment (excesses in which preceded the tech wreck) and residential property investment (excesses in which preceded the GFC) are around their long-term averages relative to GDP.

Source: Bloomberg, AMP Capital

-

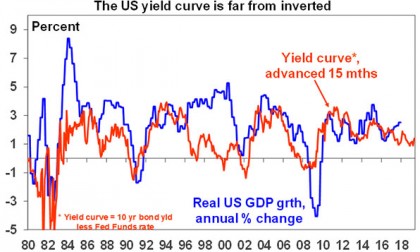

capacity utilisation is rising and inflationary pressures are building in the US but inflation is not a problem yet and it’s not an issue in other major countries. Core inflation in major countries ranges between 0.3% in Japan to 1.5% in the US.

Third, while tax cuts and additional public spending following the relaxation of spending caps will boost US growth they will take time to flow through and cause the economy to overheat.

Source: Bloomberg, AMP Capital

What to watch?

Investment implications

More volatility should be anticipated, and the fickleness of investor confidence means we can’t rule out another crash like in 1987. But despite this we still appear to be a fair way from the peak in the investment cycle so the trend in share markets likely remains up. Non-US shares and economies are less advanced in their cycles and provide opportunities for investors.

Source: AMP Capital 21 Feb 2018

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.