For the last two decades, advanced country central banks have been focussed on price stability and have played the first line of defence in stabilising the economic cycle whereas fiscal policy has played back up, focussing more on fairness and efficiency. This same approach has been applied since the global financial crisis with fiscal policy relegated to the back seat since 2010 because growth hadn’t collapsed and there has been a desire to stabilise public debt. But we are starting to see debate about whether a new approach is needed. The issue has been highlighted by San Francisco Fed President John Williams.1

Why the debate?

Several factors are driving this debate including:

-

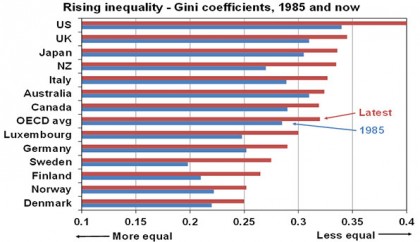

Concerns that too much is being asked of monetary policy in the face of structural factors that may be depressing growth. These include aging populations, high private sector debt levels, rising levels of inequality (as high income earners save more of their income than low income earners – so a greater share of income going to high income earners means slower economic growth) and low levels of investment in an increasingly “capital lite” economy.

Data is after taxes and welfare transfers. Source: OECD, AMP Capital

-

A fall in the natural (or equilibrium) rate of interest as slower population and productivity growth drive slower potential economic growth.

-

Concerns that central banks may be scraping the bottom of the barrel in terms of useful monetary policy tools. The dubious experience with negative interest rates in Europe and Japan are an obvious example. (I struggle to see why anyone would want to lend or invest with a negative interest rate. It’s a disaster for those that have no choice such as European insurance companies or pension funds,).

-

Concerns that relying too much on easy monetary policy may contribute to rising inequality as low interest rates disproportionally harm lower income earners but higher share markets help high income earners.

Monetary policy has worked

For what it’s worth, my view is that ultra easy monetary policy has worked during the last few years.

-

In the absence of aggressive monetary easing, advanced countries would likely have faced depression, deep deflation and a complete financial meltdown after the GFC.

-

On virtually all metrics – confidence, employment, unemployment, underemployment, consumer spending, business investment, bank lending, core inflation – the US economy has improved significantly in recent years. And the household savings rate has fallen from its post-GFC high.

-

Similarly in Australia, the fall in interest rates since 2011 has helped the economy rebalance in the face of collapsing mining investment: via a pick-up in housing construction and growth in consumer spending. While those close to retirement may be saving more because of lower investment returns, the household saving rate overall has drifted down from 11% to around 8% since the first RBA rate cut in 2011. And the RBA rate cuts have helped push the $A lower, which has helped sectors like tourism and higher education.

-

Japan and Europe have been less successful – perhaps because they were slower and less aggressive in easing initially. But even so, core inflation in both regions is up from its lows and unemployment has been falling.

-

And much of the threat of deflation in recent years has been due to the plunge in commodity prices – which is mainly due to a surge in their supply – rather than any failure of easy monetary policy. This looks to have largely run its course.

However, it is right to ask whether too much is being asked of monetary policy.

Monetary versus fiscal policy

There are several aspects to this debate. First, some have suggested – mostly in Australia – that inflation targets should just be lowered but this “changing the goal post” approach will just lock in very low inflation and leave us vulnerable to deflation in the next downturn. Falling prices can be good if it reflects high productivity and where wages growth is strong. But in the current environment of high debt levels, it would most likely be bad because it would make it harder to service debt and further threaten economic growth. So lowering inflation targets makes no sense.

Second, it’s been suggested that the approach to inflation targeting should be changed to either a higher inflation rate target (as this might make achieving a lower real official rate of interest easier – eg getting a real interest rate of -3% if that is needed to boost the economy is much easier if inflation is 3% than if it is 2%) or switch to targeting either price levels or nominal GDP levels (which would mean that if there is underachievement in one period it would have to be made up in the next). While these sound nice in theory, they remind me of the joke about an economist on a deserted island with a can of baked beans who assumes he has a can opener. Neither approach actually gets inflation up.

Third, another approach is to adopt a larger role for government spending and taxation policy in areas that enhance economic growth, like infrastructure, in measures to reduce inequality and in terms of more countercyclical spending (such as public spending that automatically ramps up with rising unemployment and falls with falling unemployment).

Finally, there are policies that combine both monetary and fiscal policy using some form of monetary financing of public spending, often called “helicopter money”. It would have the benefit of a much bigger spending payoff than quantitative easing (much of which just sat in bank reserves), the spending could be targeted to reach fairness objectives and it could be wound back when inflation objectives are met.

Issues and constraints

Of these, the measures involving a greater role for fiscal policy make more sense. As noted, lower inflation targets would make no sense. Higher inflation targets have merit and it’s worth noting that when Australia introduced its relatively high (by New Zealand standards!) inflation target of 2-3% over 20 years ago, it was partly motivated by a desire for flexibility on the downside. So there is a case for the 2% targets in the US, Japan and Europe to be revised to 2-3% just like Australia!

Similarly price level or nominal GDP level targeting has merit. But a central bank targeting nominal GDP does leave it with too much responsibility for real GDP growth and could lead to years where, say, a nominal growth target of 5% is met but it’s made up of too much inflation. More broadly, as noted earlier, all these ideas do little to actually push inflation up.

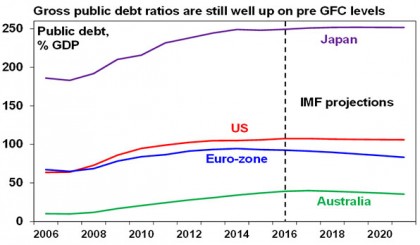

Which brings us to a greater role for fiscal policy. An obvious constraint here is that public debt to GDP ratios remain way up from pre GFC levels – and in fact in most countries have increased over the last few years – despite several years of austerity. This can be seen in the next chart.

Source: IMF, AMP Capital

However, there is a danger in pushing this argument too far as fiscal austerity and the lack of fiscal stimulus so far this decade may be depressing nominal GDP growth and making it harder to reduce public debt to GDP ratios in advanced countries.

Well targeted public spending focussed on infrastructure, improving access to education and using tax policy to lower inequality could help boost nominal GDP growth.

Australia – via the Asset Recycling Initiative introduced by former Treasurer Joe Hockey – has shown that infrastructure spending can be boosted by privatising existing state-owned assets and recycling the proceeds into new infrastructure spending. This is helping to boost growth without actually adding to public debt.

However, where that is not possible or more radical action is needed, the best approach would be a coordinated use of monetary and fiscal policy. Quantitative easing programs which have depressed bond yields have arguably already given governments more latitude to expand fiscal policy because they can borrow at very cheap rates. Of course an objection is that it hasn’t technically reduced public debt levels so households or businesses may not respond much to any resultant fiscal stimulus because they think it will be replaced with tax hikes down the track (a phenomenon known as Ricardian Equivalence). A way around this of course is helicopter money. This could involve a government issuing perpetual bonds with a zero rate of interest (and hence no value) to the central bank or the central bank effectively cancelling some of the public debt it holds. Either way, a fiscal expansion – eg directly putting cash into the hands of low and middle income households – could be undertaken with no increase in public debt.

Will we get there?

There is already plenty of evidence of a shift away from fiscal austerity and towards fiscal stimulus: the European Commission is effectively ignoring budget deficit overruns by Spain and Portugal; in shifting to more “inclusive” policies, UK PM Theresa May is ditching plans for more fiscal tightening; in the US, Hillary Clinton and Donald Trump have been promising more infrastructure spending whereas in the 2012 campaign it was all about getting the budget deficit down. If mainstream politicians are too survive the populist backlash against economic rationalism, they will probably have little choice but to embark on more expansionary fiscal policies.

However, helicopter money looks a long way off (if at all) in the US, which looks close to achieving its inflation target. And in Australia it’s not an issue at all. While there has been some talk of quantitative easing in Australia I can’t see the case for it as business conditions are reasonable, the slump in mining investment will start to abate in 2017-18 just as housing investment tops out, and public investment looks like it will be strong in the years ahead. (And, as indicated in the first chart, the deterioration in income inequality in Australia over the last 30 years is marginal once the tax and welfare system is taken into account, which suggests less urgency to act on inequality.)

However, there is a stronger case for helicopter money in Japan as core inflation has been falling lately with the risk of a return to deflation and public debt ratios are extreme.

Implications for investors

For investors, a shift in emphasis away from monetary policy and towards a greater role for fiscal policy could be positive if it boosts inflation and nominal growth. This would mean bond yields will start to bottom out and drift higher over time, but it could help growth assets like property and shares to the extent that it boosts profit and rental growth.

1 See John C. Williams, “Monetary Policy in a Low R-star World,” FRBSF Economic Letter, August 2016

Source: AMP Capital

About the Author

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.