– but falling confidence and home prices will limit RBA tightening

Dr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP Capital

Key points

-

The RBA has hiked the cash rate again – by 0.5% taking it to 0.85% and continues to signal more rate hikes ahead.

-

We expect the cash rate to rise to 1.5-2% by year-end and to peak at 2-2.5% by mid next year.

-

Greater sensitivity to higher interest rates will cap how much the RBA ultimately needs to hike by well below market expectations for a cash rate of 4% or more.

-

Falling home prices and very weak consumer confidence indicate RBA monetary tightening is already getting traction earlier than in past rate hiking cycles.

Introduction

The RBA has increased its official cash rate by another 0.5% taking it to 0.85% for the second rate hike in this cycle. This was above market expectations. Our expectation was for a 0.4% hike with the risk that it would be 0.5%.

In justifying the move the RBA noted that: the economy is resilient; the labour market is strong with the unemployment rate falling to just 3.9%; the Bank’s business liaison continues to point to higher wages growth; and inflation is expected to increase even more than it expected a month ago with notably higher prices for electricity, gas and petrol.

The RBA’s move is consistent with the stepped up pace of tightening from central banks in New Zealand and Canada and likely soon in the US as they all try to get ahead of the surge in inflation and to contain inflation expectations. This and the low starting point explains why the 0.5% rate hike is the biggest in 22 years.

The RBA’s commentary remained hawkish reiterating that it will “do what is necessary” to return inflation to target and that this will likely require “further steps in the process of normalising monetary conditions” which in short means that more interest rate hikes are likely on the way.

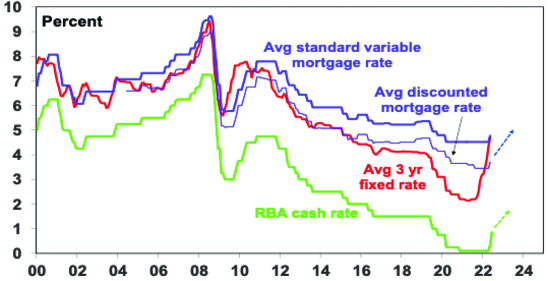

Australian interest rates on the rise

Source: RBA, Bloomberg, AMP

Banks are likely to pass the RBA’s rate hike on in full to their variable rate customers and deposit rates will rise further. Fixed mortgage rates have already moved up in line with rising bond yields in anticipation of higher cash rates – more than doubling from record lows around 2% early last year.

While the rate hike adds to the cost of living the RBA has little choice but to “normalise” interest rates

Supply constraints – reflecting the impact of the pandemic, the war in Ukraine and the floods – are the main factor behind the rise in inflation and RBA rate hikes won’t boost supply. But the RBA has little choice but to continue the process of tightening monetary policy.

-

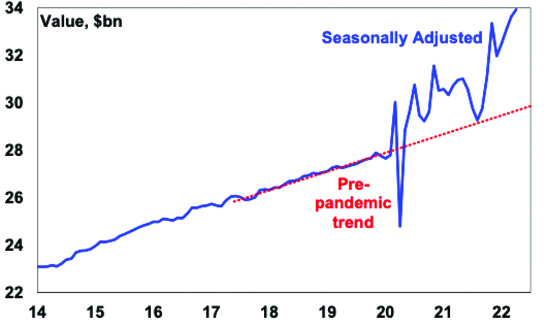

First, strong Australian demand is also a factor with for example retail sales still running around 15% above their long-term trend. As is the very tight labour market.

Australian retail sales

Source: ABS, AMP

-

Second, having a still near zero cash rate when unemployment is 3.85% and inflation is 5% and still rising makes no sense. So the RBA is right to be “normalising monetary conditions”.

-

Third, inflation pressures are still building with surging electricity and gas prices, petrol back above $2 a litre, rents starting to rise rapidly and supermarkets warning of more price rises and increasing wage demands. Its looking likely that inflation will now rise to 7% or so in the second half (compared to RBA expectations for a peak around 6%).

-

Fourth, the experience from the 1960s and 1970s tells us the longer high inflation persists the more inflation expectations will rise and get built into price and wage setting making it even harder to get inflation back down again without a recession. By raising rates the RBA is signalling its commitment to get inflation back down to the 2-3% target. Not doing so would call that commitment into question which would see inflation expectations rise.

-

Finally, the global backdrop now of bigger government, a long period of ultra-easy monetary policy and big budget deficits, the reversal in globalisation and the demographic decline in the proportion of workers relative to consumers, all point to a transition from the falling and low inflation world of the last 30-40 years to structurally higher inflation. This means that central banks like the RBA have to be more hawkish than has been the case for some time.

Money market expectations for a cash rate of 4% plus are too hawkish.

All of the above considerations point to more rate hikes ahead. But trying to get a handle on where they peak is always a bit of a guessing game. A build up in excess household saving of around $250bn through the pandemic – which is evident in a 25% rise in bank deposits since late 2019 and many households being well ahead on their mortgage payments – imparts a degree of resilience for households which some have argued means that the RBA may have to be a lot more aggressive taking the cash rate to 3.5% or more. This along with the hawkish nature of the RBA’s post meeting statement this month appears to underpin futures market expectations for the cash rate to rise above 3% by year end and then 4.5% by mid next year and to then stay above 4% for the subsequent two years.

However, its likely that the cash rate won’t have to go that high before the RBA achieves its aim of cooling demand enough to take pressure off inflation and keep inflation expectations down.

-

First, while the household debt situation is not as perilous as some would have it – with household wealth up more than household debt and many households well ahead on their payments – many will experience a significant amount of pain from higher rates. For example, RBA analysis indicates that about 25% of variable rate borrowers would see a 30% or more rise in mortgage payments from a 2% rise in rates. A new borrower in NSW where average new loans are around $800,000 would see monthly payments jump by more than $1000 if the cash rate rose to 2.5% compared to what they were paying back in March. This is a huge hit to the household budget.

-

Second, the RBA just wants to slow things down to take pressure off inflation and give time for supply to catch up. It does not want to crash the economy and is not on autopilot. So it will be watching indicators of spending and things like house prices very closely.

-

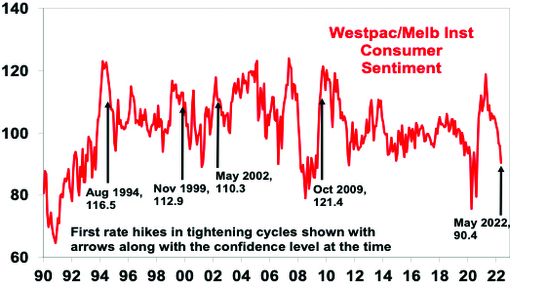

Third, it looks like the RBA is already getting traction. Consumer confidence has fallen sharply and is well below where it’s been at the start of past RBA rate hiking cycles. See the next chart.

Consumer confidence

Source: Westpac/MI, AMP

National average home prices have already started to fall, whereas at the start of previous RBA rate hiking cycles they were rising solidly and did not start falling until sometime after the start of rate hikes. See the next chart

Capital city home prices

Source: Core Logic, AMP

The earlier than normal hit to confidence and home prices likely reflects a combination of things: a greater sensitivity to interest rate movements now reflecting higher levels of household debt (and high levels of debt required to get into the property market for new borrowers); the fact that the tightening cycle started before the rise in the cash rate this time around with the removal of the 0.1% bond yield target last year which helped drive a sharp rise in fixed mortgage rates and pulled the rug out from under the housing boom before the RBA started to move the cash rate; and cost of living pressures that have seen an unprecedented plunge in real wages and hence spending power in the context of the last 20 years.

Australian wages

Source: ABS, AMP

But regardless of the precise drivers, the bottom line is that RBA monetary tightening appears to be getting traction earlier than would normally occur in an interest rate tightening cycle. While the RBA does not target house prices, falling home prices (where we expect a 10 to 15% top to bottom fall) will weigh on consumer spending (via negative wealth effects as we saw in 2017-18). All of which will start to take pressure off inflation and limit the amount by which the RBA ultimately will need to raise the cash rate by. So we expect that while the RBA will raise the cash rate to 1.5% to 2% by year end, the peak in the cash rate will come at around 2% to 2.5% by mid next year. This is well below money market expectations for a rise above 4%.

Given that the latest RBA hike was roughly in line with our expectations we have made no changes to our cash rate forecasts. We continue to see average home prices falling 10-15% over the next 18 months but this may now occur earlier and faster than previously expected.

Source: AMP Capital June 2022

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.