Introduction

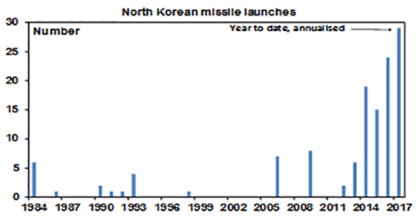

Tensions with North Korea have been waxing and waning for decades now but in recent times the risks seem to have ramped up dramatically as its missile and nuclear weapon capabilities have increased. The current leader since 2011, Kim Jong Un, has launched more missiles than Kim Il Sung (leader 1948-1994) and Kim Jong Il (1994-2011) combined.

Tensions with North Korea have been waxing and waning for decades now but in recent times the risks seem to have ramped up dramatically as its missile and nuclear weapon capabilities have increased. The current leader since 2011, Kim Jong Un, has launched more missiles than Kim Il Sung (leader 1948-1994) and Kim Jong Il (1994-2011) combined.

Source: CNN, AMP Capital

The tension has ramped up particularly over the last two weeks with the UN Security Council agreeing more sanctions on North Korea and reports suggesting North Korea may already have the ability to put a nuclear warhead in an intercontinental ballistic missile that is reportedly capable of reaching the US (and Darwin).

US President Trump also threatened North Korea with “fire, fury and, frankly, power” only to add a few days later that that “wasn’t tough enough” and “things will happen to them like they never thought possible” and then that “military solutions…are locked and loaded should North Korea act unwisely”. Meanwhile, North Korea talked up plans to fire missiles at Guam before backing off with Kim Jong Un warning he could change his mind “if the Yankees persist in their extremely dangerous reckless actions”.

This is all reminiscent of something out of James Bond (or rather Austin Powers) except that it’s serious and naturally has led to heightened fears of military conflict. As a result, share markets dipped last week and bonds and gold benefitted from safe haven demand, although the moves have been relatively modest and markets have since bounced back.

At present there are no signs (in terms of military deployments, evacuation of non-essential personnel, etc) that the US is preparing for military conflict and it could all de-escalate again, but given North Korea’s growing missile and nuclear capability it does seem that the North Korean issue, after years of escalation and de-escalation, may come to a head soon. It’s also arguable that the volatile personalities of Kim Jong Un and Donald Trump and the escalating war of words have added to the risk of a miscalculation – eg where North Korea fires a missile into international waters, the US seeks to shoot it down, which leads to a cycle of escalating actions. This note looks at the implications for investors.

Shares and wars (or threatened wars)

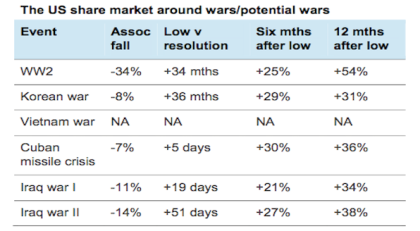

Of course there have been numerous conflicts that don’t even register for global investors beyond a day or so at most if at all. Many have little financial market impact because they are not seen as having much economic impact (eg the war in Afghanistan in contrast to 1991 and 2003 wars with Iraq, which posed risks to the supply of oil). As such, I have only focussed on the major wars/potential wars since World War 2 and only on the US share market (S&P 500) as it sets the direction for others (including European, Asian and Australian shares).

-

World War 2 (September 1939-September 1945) – US shares fell 34% from the outbreak of WW2 in September 1939, with 20% of this after the attack on Pearl Harbour, and bottomed in April 1942. This was well before the end of WW2 in 1945. Six months after the low, shares were up 25% and by the time WW2 had risen by 108%.

-

Korean War (June 1950-July 1953) – US shares initially fell 8% when the war started but this was part of a bigger fall associated with recession at the time. Shares bottomed well before the war ended and trended up through most of it.

-

Vietnam War (1955-1975) – For most of this war US shares were in a secular bull market but with periodic bear markets on mostly other developments. Rising inflation and a loss of confidence associated with losing the Vietnam war may have contributed to the end of the secular bull market in the 1970s – but the war arguably played a small role in this.

-

Cuban Missile Crisis (October 1962) – Shares initially fell 7% over eight days as the crisis erupted but this was part of a much bigger bear market at the time. They bottomed five days before it was resolved and then rose sharply. This is said to be the closest the world ever came to nuclear war

-

Iraq War I (August 1990-January 1991) – Shares fell 11% from when Iraq invaded Kuwait to their low in January 1991 but again this was part of a bigger fall associated with a recession. Shares bottomed 8 days before Operation Desert Storm began and 19 days before it ended and rose sharply.

-

Iraq War II (March-May 2003) – Shares fell 14% as war loomed in early 2003 but bottomed nine days before the first missiles landed and then rose substantially although again this was largely due to the end of a bear market at the time.

Source: AMP Capital

The basic messages here are that:

-

Shares tend to fall on the initial uncertainty but bottom out before the crisis is resolved (militarily or diplomatically) when some sort of positive outcome looks likely;

-

Six months after the low they are up strongly; and

-

The severity of the impact of the war/threatened war on shares can also depend on whether they had already declined for other reasons. For example, prior to World War 2, the Cuban Missile Crisis and the two wars with Iraq, shares had already had bear markets. This may have limited the size of the falls around the crisis.

Possible scenarios

In thinking about the risks around North Korea, it’s useful to think in terms of scenarios as to how it could unfold:

-

Another round of de-escalation – With both sides just backing down and North Korea seemingly stopping its provocations. This is possible, it’s happened lots of times before, but may be less likely this time given the enhanced nature of North Korea’s capabilities.

-

Diplomacy/no war – Sabre rattling intensifies further before a resolution is reached. This could still take some time and meanwhile share markets could correct maybe 5-10% ahead of a diplomatic solution being reached before rebounding once it becomes clear a peaceful solution is in sight. An historic parallel is the Cuban Missile Crisis of 1962 that saw US shares fall 7% and bottom just before the crisis was resolved, and then stage a complete recovery.

-

A brief and contained military conflict – Perhaps like the 1991 and 2003 Iraq wars proved to be, but without a full ground war or regime change. In both Iraq wars while share markets were adversely affected by nervousness ahead of the conflicts, they started to rebound just before the actual conflicts began. However, a contained Iraq-style military conflict is unlikely given North Korea’s ability to launch attacks against South Korea (notably Seoul) and Japan.

-

A significant military conflict – If attacked, North Korea would most likely launch attacks against South Korea and Japan causing significant loss of life. This would entail a more significant impact on share markets with, say, 20% or so falls (more in Asia) before it likely becomes clear that the US would prevail. This assumes conventional missiles – a nuclear war would have a more significant impact.

Of these, diplomacy remains by far the most likely path. The US is aware of the huge risks in terms of the likely loss of life in South Korea and Japan that would follow if it acted pre-emptively against North Korea and it retaliates, and it has stated that it’s not interested in regime change there. And North Korea appears to only want nuclear power as a deterrent. In this context, Trump’s threats along with the US show of force earlier this year in Syria and Afghanistan are designed to warn North Korea of the consequences of an attack on the US or its allies, not to indicate that an armed conflict is imminent. Rather, comments from US officials it’s still working on a diplomatic solution. As such, our base case is that there is a diplomatic solution, but there could still be an increase in uncertainty and share market volatility in the interim. Key dates to watch are North Korean public holidays on August 25 and September 9, which are often excuses to test missiles, and US-South Korean military exercises starting August 21.

Correction risks

The intensification of the risks around North Korea comes at a time when there is already a risk of a global share market correction: the recent gains in the US share market have been increasingly concentrated in a few stocks; volatility has been low and short-term investor sentiment has been high indicating a degree of investor complacency; political risks in the US may intensify as we come up to the need to avoid a government shutdown and raise the debt ceiling next month, which will likely see the usual brinkmanship ahead of a solution (remember 2013); market expectations for Fed tightening look to be too low; tensions may be returning to the US-China trade relationship; and we are in the weakest months of the year seasonally for shares. While Australian shares have already had a 5% correction from their May high, they are nevertheless vulnerable to any US/global share market pull back.

However, absent a significant and lengthy military conflict with North Korea (which is unlikely), we would see any pullback in the next month or so as just a correction rather than the start of a bear market. Share market valuations are okay – particularly outside of the US, global monetary conditions remain easy, there is no sign of the excesses that normally presage a recession, and profits are improving on the back of stronger global growth. As such, we would expect the broad rising trend in share markets to resume through the December quarter.

Implications for investors

Military conflicts are nothing new and share markets have lived through them with an initial sell-off if the conflict is viewed as material followed by a rebound as a resolution is reached or is seen as probable. The same is likely around conflict with North Korea. The involvement of nuclear weapons – back to weapons of mass destruction! – adds an element of risk but trying to protect a portfolio against nuclear war with North Korea would be the same as trying to protect it against a nuclear war during the Cold War, which ultimately would have cost an investor dearly in terms of lost returns. While there is a case for short-term caution, the best approach for most investors is to look through the noise and look for opportunities that North Korean risks throw up – particularly if there is a correction.

If you would like to discuss anything in this report, please call us on 02 9299 1500.

Source: AMP Capital 15 August 2017

Author

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.