Introduction

It’s nearly four years since the tumultuous 2020 US presidential election and now the next one is almost upon us. So far investment markets have paid little attention to it or have just focussed on the upside (lower taxes and less regulation) if Trump returns. But that may change as it draws near – with the first debate scheduled for 27 June and with a Trump victory running the risk of weakening US democracy and US global alliances and threatening a big ramp up in protectionism and a further reversal in free trade. Being unable to run for a third term, a second Trump presidency will lack the electoral constraints of his first term (which led to the Phase One trade deal with China) and is likely to have less “adults in the room”.

Polls have Biden trailing

-

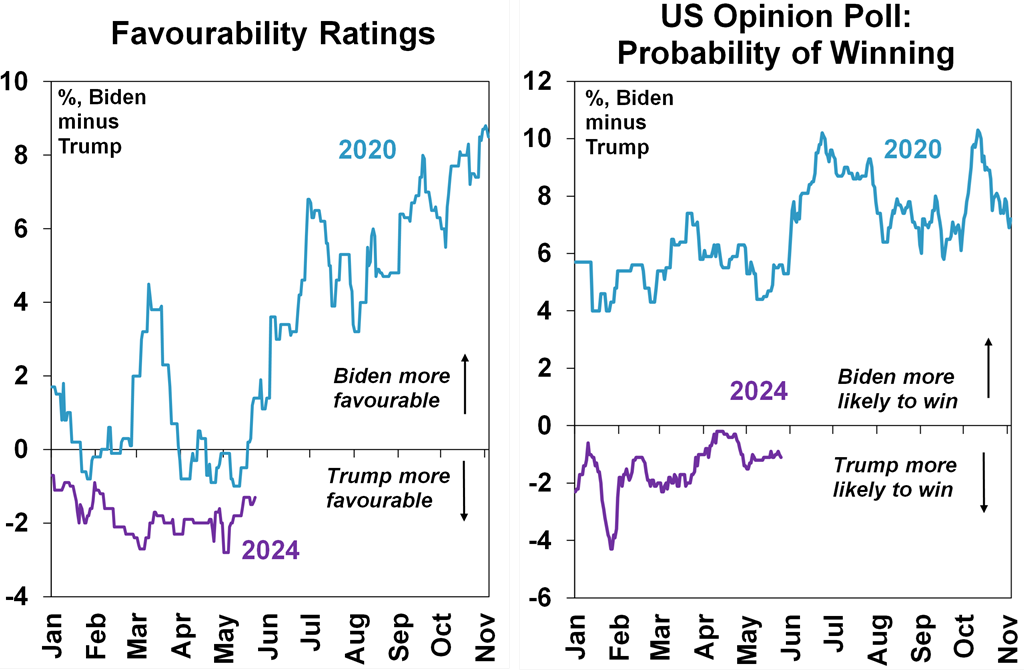

Real Clear Politics poll average has Biden trailing Trump by 1 to 2 points in terms of favourability and presidential voting intentions. This is well behind where he was at the same point in 2020. See next chart.

Source: Real Clear Politics, Bloomberg, AMP

-

Biden also lags Trump by around 1 to 9 points in key battleground states, whereas he was leading at this point in 2020.

-

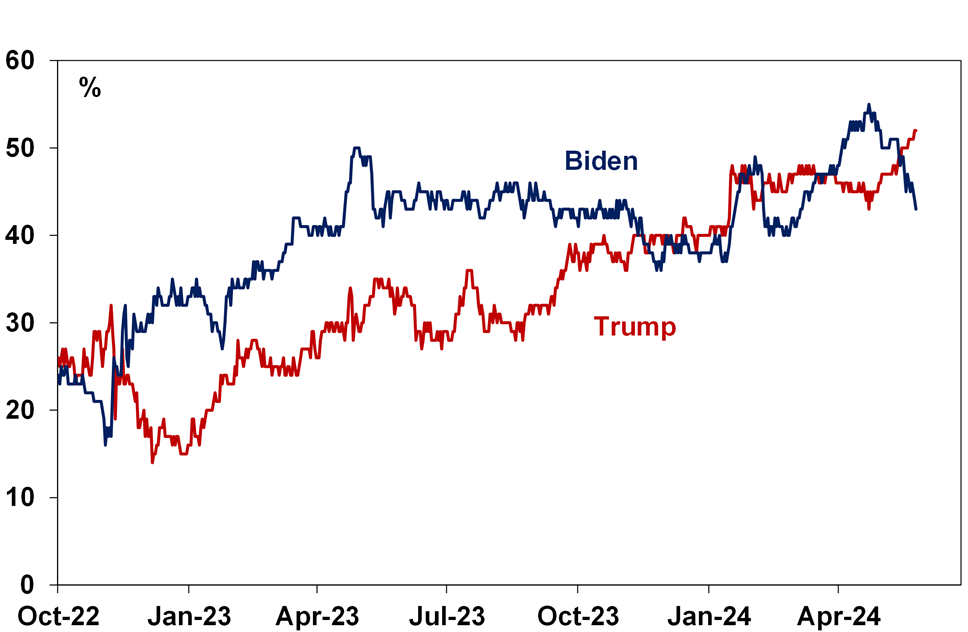

The ‘PredictIt’ betting market has Trump on 51% probability of winning versus Biden on 44%, having just crossed over from favouring Biden.

-

If Trump wins, it’s likely the Republicans would regain control of the Senate (where they have an edge as the Democrats need to defend more seats) and keep the House, resulting in a clean sweep.

Betting markets’ probability of winning

Source: PredictIt, AMP

“It’s the economy, stupid”

However, there are still 5 months to go so it’s too early to write Biden off. First, the historical record indicates incumbent presidents tend to be re-elected if there is no recession in the two years before the election. Since 1932, all incumbents seeking re-election have failed if this was not the case. While leading indicators point to a high risk of recession, so far the economy has been strong. But how it behaves up to November is critical.

US presidential elections if recession in prior 2 years and incumbent up for re-election

|

President |

Election year |

Recession |

Re-elected? |

|

Trump |

2020 |

Yes |

No |

|

Obama |

2012 |

No |

Yes |

|

Bush Jr |

2004 |

No |

Yes |

|

Clinton |

1996 |

No |

Yes |

|

Bush Snr |

1992 |

Yes |

No |

|

Reagan |

1984 |

No |

Yes |

|

Carter |

1980 |

Yes |

No |

|

Ford |

1976 |

Yes |

No |

|

Nixon |

1972 |

No |

Yes |

|

Johnson |

1964 |

No |

Yes |

|

Eisenhower |

1956 |

No |

Yes |

|

Truman |

1948 |

No |

Yes |

|

Roosevelt |

1944 |

No |

Yes |

|

Roosevelt |

1940 |

No |

Yes |

|

Roosevelt |

1936 |

No |

Yes |

|

Hoover |

1932 |

Yes |

No |

|

Coolidge |

1924 |

Yes |

Yes |

|

Wilson |

1916 |

No |

Yes |

|

Taft |

1912 |

Yes |

No |

|

McKinley |

1900 |

Yes |

Yes |

Source: Strategas, AMP

Second, normally around July in the election year incumbent presidents start to see an upswing in support.

Third, polls indicate that roughly 14% are undecided and they often don’t make up their minds until the end of the party conventions (July/August).

Fourth, around 20-25% of Trump supporters indicate that they will reconsider if he is convicted of a crime. Of course, several of the stronger cases against him have been delayed likely leaving the arguably less threatening for Trump New York “hush money” case.

Finally, while third party candidate Robert F Kennedy is more of a threat to Biden than Trump, it’s likely he will be convinced to exit the race.

Of course, it can all blow the other way if there is a surge in oil prices (e.g. if the Israel war expands to include Iran and Russia curtails its energy exports in the hope it will support Trump who as president will cut support for Ukraine) and the economy slides into recession.

Key Trump policy differences versus Biden

Taxation: Trump would look to make the 2017 corporate and personal tax cuts (which took the corporate rate to 21% and the top marginal tax rate to 37%) permanent (as they expire in 2025 which would result in higher taxes under Biden) and to lower them possibly further.

Trade: Trump is threatening to impose a 10% tariff on all imports and a 60% tariff on all imports from China. This would take the average US tariff rate from around 2.5% to around 17%, far surpassing the 3% peak seen in Trump’s first term. This may be “maximum pressure” bluster, but while “we shouldn’t take him literally, we should take him seriously.” Biden has basically maintained Trump’s China tariffs and recently announced he will add to them (but only on 4% of imports from China) and has dramatically ramped up subsidies for manufacturing in America. This is part of a broader global trend towards protectionism and deglobalisation. Trump (who sees the US trade deficit as a sign that America is being ripped off) would likely dramatically ramp this up accelerating the process of deglobalisation and adding to the likelihood of global trade wars as other countries retaliate on a far bigger scale than in 2018-19 and without political considerations getting in the way (as he can’t have a third term).

Immigration: Immigration has surged under Biden making it a big issue and Trump will likely aggressively curtail both legal and illegal immigration.

Fed independence: Trump would seek to replace Jerome Powell and his supporters are looking at ways to roll back the Fed’s independence.

Climate policy: Trump will likely reverse the US’ net zero commitments and most of the policies Biden introduced to support it. Subsidies for green manufacturing are likely to be replaced with wider industry subsidies.

Regulation: Trump is likely to slash regulation particularly benefitting the energy and financial sectors.

Budget deficit: The deficit remains huge (at 6.3% of GDP) owing to big government spending. It would likely get bigger under Trump’s tax policies.

Economic impact of a Trump victory

Trump’s policies in support of tax cuts and deregulation could help boost the supply side of the US economy via a boost to productivity (which is already on the mend and will be helped by the rapid take up of AI in the US). However, on balance Trump’s policies – with higher tariffs and hence higher import prices, sharply lower labour force growth and moves to weaken the Fed’s inflation fighting credentials – will likely add to inflation.

There is also a risk that a higher budget deficit, with no sign of improvement at a time when US public debt is now very high (at 125% of GDP), will result in a market backlash and higher bond yields. Furthermore, his brinkmanship and erratic policy making style is likely to add to policy uncertainty which could hamper business investment.

A lot will depend on the sequencing of his policy moves. If he runs with tax cuts first it could boost the economy in say 2025, but if he runs first with sharp tariff hikes, immigration cuts & an attack on the Fed it could be taken more negatively early on. In 2017 he ran with the positives first to help shore up the economy, but this time around he may run with negatives first as there will be no constraint from the desire to win another election.

Likely market reaction

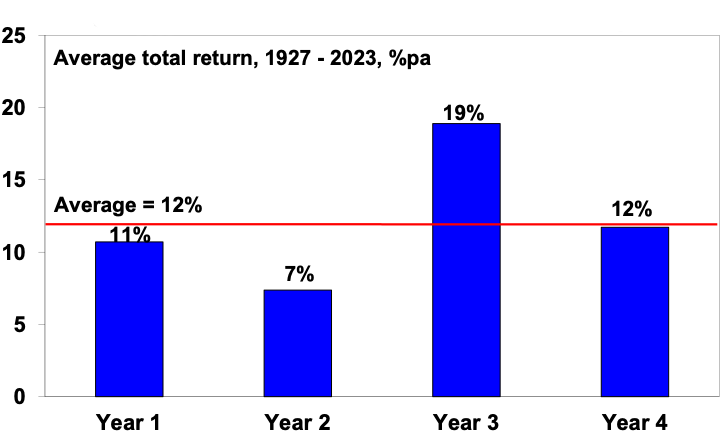

Firstly, despite the heightened policy uncertainty the election year is normally an okay year for US shares. Since 1927, the election year, or year 4 in the presidential cycle, has had a return of around 12%.

US sharemarket returns through the presidential cycle

Source: Bloomberg, AMP

Second, the run up to the election will likely see increased share market volatility if Trump remains ahead and investors start to focus on the risks of a new trade war, a hit to the US labour force and to the Fed under Trump. After Trump’s victory in 2016 shares soared 38% to January 2018 as the focus in his first year was on business-friendly tax cuts and deregulation but they fell in 2018 as the focus shifted to trade wars. So, if there is a Trump victory, the share market’s reaction in the first 6-12 months will be heavily influenced by his sequencing of tariff hikes versus tax cuts.

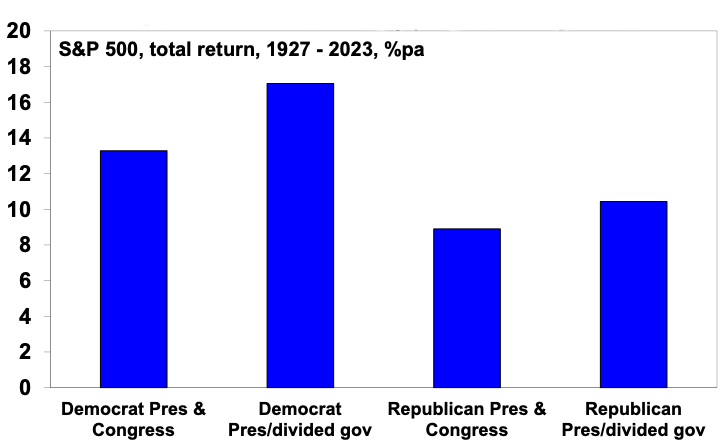

Third, historically US shares have done best under Democrat presidents with an average return of 14.4% pa since 1927 compared to an average return under Republican presidents of 10% pa. However, the best average result has actually occurred when there has been a Democrat president and Republican control of the House, the Senate or both and the worst average return has been when there’s been a clean Republican sweep.

US share market returns by political configuration

Source: Bloomberg, AMP

Finally, a Trump presidency would likely mean higher bond yields (with somewhat higher inflation and budget deficits) and a higher $US (partly reflecting higher global economic uncertainty and the impact of US tariffs).

Implications for Australia

As a relatively open economy with high trade exposure to China, Australia would be vulnerable to an intensification of global trade wars as a result of a Trump victory, particularly if it weighs on demand for Chinese exports. An OECD study showed that Australia could suffer a 1.2% reduction in GDP as a result of a 10% reduction in global trade between major countries. This is second only to Korea in OECD countries and reflects Australia’s high exposure to China. Resources shares would be most at risk and the $A would likely fall. Of course, similar fears existed during the last Trump trade war, and it didn’t turn out so bad. Much would depend on how other countries respond and how hard Trump goes. And of course, Trump may not win!

Dr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP

Source: AMP Capital May 2024

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.