The disappointing retail sales figures from the last quarter could be just the tip of the iceberg for those watching the retail sector heading into Christmas, reckons Dermot Ryan, AMP Capital’s Portfolio Manager – Australian Equities.

But it’s not likely to be the so called “Amazon effect” of internet shopping, nor competition from fast fashion retailers, or even unfavourable currency swings Ryan is factoring in when he’s calling out the possibility we’re heading for a flat Christmas in terms of spending and economic growth – although all three of these factors could prove to be head winds for retailers but a boon for shoppers.

It’s the debt overhang from the housing boom that could end up casting the longest and coldest shadow over Australia’s Christmas cheer, Ryan says, pointing out he’s reading the data and not himself the Christmas Grinch.

“We’re at the mature stage of a housing cycle where a lot of mortgagees have large debts and some groups have overextended themselves buying property. Even before the RBA (Reserve Bank of Australia) thinks about raising interest rates this year, stresses are appearing as banks raise the cost of interest only and investor loans and I’m guessing it will seriously curtail their ability to spend this festive season,” Ryan explains.

Much has been said and written about the challenges facing retailers, firstly stemming from new competition coming to Australia, and secondly as technology facilitates better price discovery which has the effect of eating into retailers’ margins.

The September quarter was the first quarterly decline in retail sales figures since 2012 and only the fourth recorded decline since the global financial crisis, according to the Australian Bureau of Statistics data released in early November.

The market had forecast a rebound in September following a steep fall in retail sales the previous month – the largest monthly decline recorded by the ABS in close to five years – but that rebound never materialised.

However, reading further into the data, Ryan believes the hefty weight of mortgage payments – which he points out Australian households remain on the hook for – have not impacted retail sales to the extent he ultimately expects they will… yet.

See, when a mortgage customer moves from an interest only mortgage to a principle and interest mortgage, there can be up to a 40 per cent increase in monthly repayments, Ryan explains. This change has a big impact on what left over at the end of the month, particularly for young families who are amongst the most indebted cohorts, he adds.

“It does seem like the increased mortgage payments are starting to make an initial dent into retail sales. This has further to play out given the mortgage rate hikes and ongoing push to switch mortgages to P&I (principal and interest) loans from interest only loans,” Ryan notes.

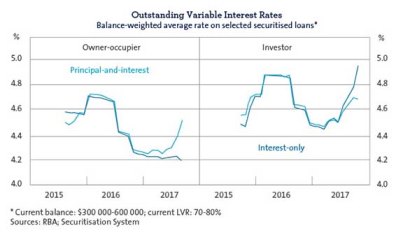

All the major banks and many of the regional institutions have raised lending rates – particularly on interest only loans – even though the RBA has kept its 1.5 per cent cash rate on hold this year.

Meanwhile, mortgagees, particularly those with interest-only loans, are already feeling the pinch, Ryan highlights.

“There are also a lot of uncontrollable cost increases for households like electricity, insurance and education that are also rising and crimping disposable income,” Ryan adds.

Cutting spending is the first thing households worried about mortgage repayments will do, Ryan says, highlighting the findings of a recent UBS study which surveyed Australians who had recently taken out a mortgage to buy a residential property.

Half of those surveyed who said they were feeling anxious about repayments said they’d cut spending while others surveyed said they’d likely opt to switch to principle and interest loans.

Switching to P&I loans increases monthly mortgage costs by 30-40 per cent which won’t be good for household spending either, Ryan highlights.

It’s clear the hangover from the housing boom and its potential impact on spending and economic growth is on the radar of the RBA too; at the latest monetary policy decision RBA Governor Philip Lowe noted “a continuing source of uncertainty is the outlook for household consumption” adding that “inflation is likely to remain low for some time, reflecting the slow growth in labour costs and increased competitive pressures, especially in retailing.”

“Looking at the data it’s clear this trend to P&I is still in play which points to a difficult Christmas ahead,” Ryan notes.

Source : AMP Capital 10 November 2017

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.