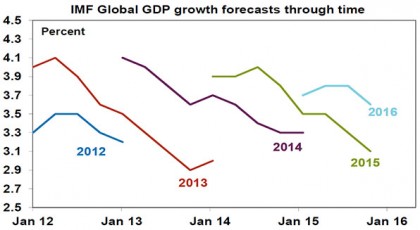

A defining feature of the economic cycle we are now going through is the constrained and fragile nature of economic growth globally. After an initial bounce post the GFC to 5.4% in 2010, global economic growth has consistently disappointed. This can be seen in the progression of the IMF’s economic growth forecasts for each year since 2012. Typically the IMF has started off looking for global growth close to 4% for the year ahead but each year has had to revise it down to around 3%, pushing the 4% bounce off into the next year. This year has been no exception – see the line for 2015 in the next chart.

Source: IMF, AMP Capital

Consequently, global growth has been continuously disappointing. It’s been the same pattern in Australia, although much of the growth slowdown in Australia owes to the ending of the mining investment boom, with a pick-up in growth back to more normal levels being constantly pushed into the future. This in turn and the fragile nature of growth has seen investors regularly questioning the post-GFC rally in shares. This note looks at why growth is so constrained and what it means.

What’s driving slow growth?

Slow and uneven growth reflects a whole range of factors.

-

It seems that we have been seeing a series of calamities acting to constrain global growth over the last few years such as the Eurozone debt crisis, Greece, the Japanese earthquake and tsunami, bouts of bad weather in the US, US debt ceiling, fiscal cliff and shutdown debacles, Ukraine, etc. Each of these should be seen as temporary but they seem to be coming with a regularity that makes them seem normal.

-

While the GFC was seven years ago now, it appears to have had a more lasting impact on confidence and particularly businesses’ desire to undertake capital investment, which has a direct constraining effect on economic growth. This likely reflects the severity of the GFC and the drip feed of post-GFC calamities.

-

Constrained capital spending has in turn been weighing on productivity growth.

-

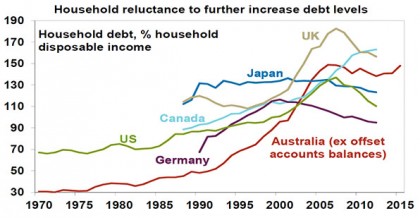

Slower growth in debt. Prior to the GFC. household debt to income ratios were trending up thanks to a combination of the increasing availability of debt and low interest rates. However, the GFC appears to have put an end to the willingness of households to take on ever higher levels of debt relative to their incomes and so we have seen debt to income ratios stabilise or decline in “Anglo” countries following an earlier lead in Japan and Germany and households running higher savings rates. While the relationship between debt and growth can be complex, this has essentially meant slower growth in consumer spending.

Source: IMF, AMP Capital

-

Rising inequality weighing on consumer spending. There is increasing concern that globalisation, offshoring and now automation are driving increasing levels of inequality in advanced countries such as the US, which in turn is weighing on consumer spending as high income households who have been benefitting are less likely to make up for lost spending from low and middle income households. This is a rather contentious point, though, and it seems to be less of an issue in Europe and Australia where social safety nets are stronger.

-

Slower labour force growth. Many countries are seeing slower population growth and in some cases falling populations, notably Japan, China and parts of Europe, but this is also the case in the US and Australia where population growth has slowed. Since an economy’s potential growth rate is determined by growth in its labour force and growth in output per hour worked (ie productivity, which has also been slowing), we have seen a slowing in potential growth. For Australia, we have revised our potential growth estimate down from 3-3.25% pa to around 2.75% pa.

-

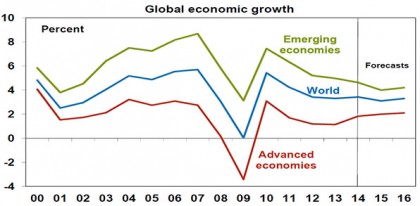

Weaker growth in emerging countries. Post the GFC, the hope was that strong growth in the emerging world would keep global growth strong. But this hasn’t happened with the downwards revisions to the IMF’s global growth forecasts increasingly being driven by the emerging world, which has been hit by a combination of a desire for more sustainable growth in China, the slump in commodity prices which is weighing on South America & a reversal in economic reform momentum in favour of old fashioned populist policies. See the next chart. In fact, half of the BRICs – Brazil and Russia – are now in recession. This is having a bigger impact globally because the emerging world is now nearly 60% of world GDP compared to less than 50% prior to the GFC.

Source: IMF, AMP Capital

There are some qualifications suggesting that the problem may not be quite as severe as it looks. In particular, rapid technological innovation may be leading to growth being understated. For example, the increasing number of “free” or low cost apps on smart devices providing services that were previously non-existent or very expensive is arguably delivering a benefit to consumers that is not properly measured resulting in the under statement of GDP growth and productivity and overstatement of inflation. It would suggest that people are doing a lot better than low wages growth suggests. This is an issue for another day but it is unlikely to be enough to fully offset the list of growth drags above.

Some of these drags should be temporary or cyclical but many are structural – slowing labour force growth, slowing productivity growth, slower growth in debt and problems in the emerging world. It’s hard to see these ending anytime soon.

The economic and financial impact of low growth

Fragile and constrained growth is having a number of impacts that are likely to persist. In particular these include:

-

Low inflation. Ongoing sub-par economic growth is seeing persistent spare capacity both in terms of unemployment and underemployment and factories not operating at their normal rate. This combined with the long-term downtrend in commodity prices in response to the surging supply of commodities is driving ongoing low inflation with periodic deflation scares. See the next chart.

-

Low interest rates. Over the long term, interest rates roughly line up with nominal economic growth. And for good reason. If real economic growth and inflation are high, nominal rates of return on investment are high and so too are interest rates and vice versa. So if inflation and real growth are low, so too should be interest rates. But there’s another factor: when economies are operating below full capacity and inflation is below target, interest rates need to run below nominal growth to hopefully boost growth and use up spare capacity. This is exactly what we have been seeing since the GFC and continue to see now. So while many simply say “low interest rates are due to central banks” the reality is that they reflect low nominal growth and spare capacity. It’s hard to see this ending soon.

Source: Thomson Reuters, AMP Capital

-

Periodic growth scares. When real economic growth is running around low levels and is fragile, periodic growth scares are likely to occur more often as the fear that adverse developments will trigger a return to recession is greater as there is less of a growth buffer. As we have seen since the GFC, these can be triggered by the normal fluctuation in economic indicators or external shocks (bad weather, military flare ups like in Ukraine, the Middle East, etc). Such growth scares keep investors nervous. So we have seen a sense of ongoing scepticism about the recovery in the global economy and in share markets that has occurred since the GFC. Investors have never quite fully bought the recovery story.

-

A longer cycle. But it’s not all negative. There is an old saying that “economic expansions don’t die of old age but of excess”. The same applies to cyclical bull markets in shares. In other words economic recessions and bear markets in shares are usually preceded by economic and/or financial imbalances such as excessive business investment, a housing boom, excessive growth in private sector debt, a build-up in inflationary pressures or unambiguously overvalued share markets. But we haven’t seen any of these as low growth has kept businesses cautious in investing, households cautious in taking on too much debt, inflation too low and investors from getting euphoric in buying shares. Sure, there are pockets of excess such as the Sydney and Melbourne home buyers’ markets but these are far from the norm globally. The absence of excess suggests we have a way to go before the next global recession or major bear market in shares.

Implications for investors

The implications for investors are simple:

-

Interest rates are likely to remain low. Sure, the Fed is itching to hike but this still looks like it could be delayed again and when it does come it is likely to be gradual and interest rate “cuts”/further monetary easing look more likely in Japan, Europe, China and Australia. This means bank deposits will remain a poor investment option except for those who can’t bear any capital loss. So the search for yield and better returns will remain.

-

Average returns are likely to be constrained as low growth means constrained return potential.

-

The cycle is likely to be longer than normal. Baring a shock – such as a major geopolitical event – the next major global economic downturn looks like being several years away yet. Which in turn suggests that the cyclical bull market in shares has a way to go.

By AMP Capital Markets 29 October 2015

About the Author

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.