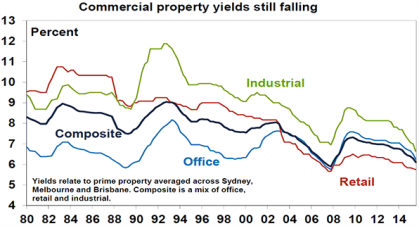

Since the end of the GFC in 2009, returns from unlisted commercial property have been strong and steady at around 9.5-10% pa. This initially reflected a recovery from the GFC related slump but more significantly a desire for decent income bearing investments from investors that has pushed down investment yields. Falling yields has been a big driver of returns as each 0.25% fall in yields translates to a 4% capital gain and since 2009 average commercial property yields have fallen from 7.3% to 6.1%. In a falling yield environment property prices move up relative to rents, providing capital gains for investors.

Source: AMP Capital

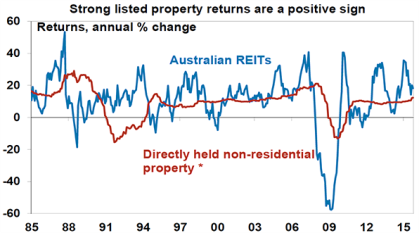

Australian Real Estate Investment Trusts (A-REITs), have been even stronger with gains of around 13% pa over the last six years. So where to from here? Has the chase for yield, at a time when concerns about rising property supply and mixed leasing conditions, gone too far or can it go further?

The demand and supply for space

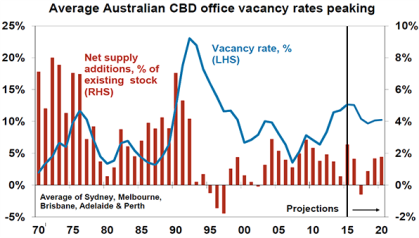

Perhaps the biggest drag is the ongoing softness in the Australian economy. While recession has been avoided and this is likely to remain the case, economic growth is likely to remain sub-par at around 2-2.5% well into next year and this is keeping unemployment relatively high, albeit less than had been feared a few years ago. This in turn is keeping a lid on space demand, particularly outside Sydney and Melbourne.

At the same time, office supply has been picking up, with particular concerns about Perth, Brisbane and Sydney with Barangaroo. However, the peak increase in supply looks like being this year and while the Perth and Brisbane markets are in in a bad way, with Perth’s vacancy looking like running around 20-25% for a few years, leasing demand has been much stronger in Sydney and Melbourne resulting in falling vacancy rates. Overall vacancy rates are likely to peak this year.

Source: AMP Capital

Rising supply is less of an issue with industrial property, but space demand has remained subdued as has also been the case in relation to retail property.

A-REITs show the way

While A-REITs are far more volatile, they provide a good lead for unlisted commercial property and their recent gains point to still solid returns ahead for unlisted property. See the next chart.

* Direct property is Mercer direct property index. Source: Bloomberg, Mercer, AMP Capital

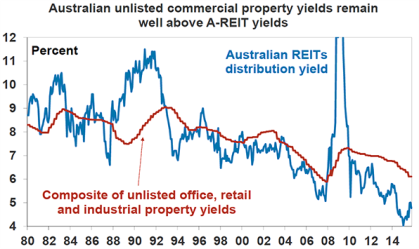

The search for yield by investors has pushed the yield on A-REITs below 5%, with the higher and more attractive unlisted commercial yields likely to continue to follow A-REIT yields lower.

Source: Bloomberg, AMP Capital

Yields remain under downwards pressure

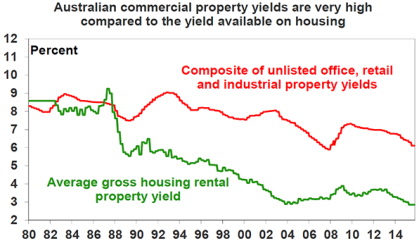

Unlisted commercial property yields also remain attractive compared to most other assets. This is particularly noticeable compared to residential property, as can be seen in the next chart. In the 1980s the rental yield on residential and commercial property (as measured by a mix of office, retail and industrial property yields) was similar, but today commercial property has an average rental yield which is far higher, ie around 6% for commercial property compared to around 3% for residential property. With Australian residential property over-valued on most measures and the strong cities of Sydney and Melbourne now starting to slow, office, retail or industrial property is far more attractive for investors than housing on a medium term horizon as it is less dependent on capital growth going forward and less at risk of a correction.

Source: REIA, AMP Capital

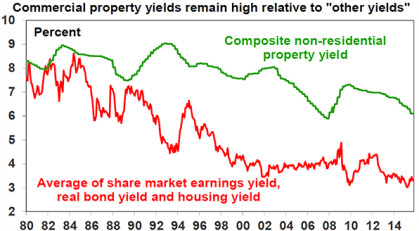

The next chart compares the yield on commercial property versus an average of government bond, equity and housing yields. The gap between commercial property yields and these yields remains wide, again suggesting yields on commercial property remain relatively attractive, despite recent falls.

Source: REIA, Bloomberg, AMP Capital

Commercial property offers a wide risk premium

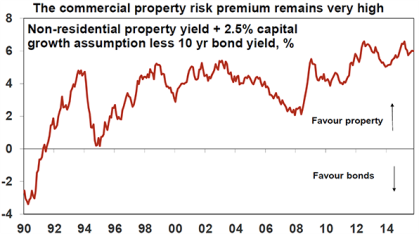

The biggest risk regarding commercial property is if bond yields back up sharply as global growth improves. However, this has been a concern for the last five years now and so far it has failed to eventuate on a sustained basis as Australian and global growth has continued to disappoint and inflation has slipped lower forcing central banks to maintain very low interest rates. In addition, the risk premium offered by commercial property over bonds remains well above average. The next chart shows a proxy for this. It assumes that rental and capital growth will average 2.5% pa over time (ie, in line with average inflation) and adds this to the average non-residential property yield to give a guide to potential total returns. The 10 year bond yield has been subtracted to show a property risk premium. While off its recent highs it remains well above its historical average.

Source: REIA, Bloomberg, AMP Capital

The bottom line is that the huge yield advantage commercial property offers over government bonds and other yield bearing assets like residential property suggests that investor demand is likely to remain strong.

Commercial property has in fact been a beneficiary of investor flows during periods of rising bond yields in the past. This happened during the bond crash of 1994 and the more gradual backup in bond yields that occurred prior to 2007 as investors simply switched out of bonds into assets like commercial property that offered higher yields at a time when leasing conditions were strong. Property only became vulnerable in 1990 and 2007 when the property risk premium in the previous chart had fallen to far less attractive levels than is currently the case and then leasing conditions deteriorated dramatically against a backdrop of rising supply.

Return outlook and what to watch

While soft leasing conditions and supply concerns in some areas (notably Perth and Brisbane offices) are likely to constrain returns, overall returns from unlisted commercial property are likely to remain strong for the next few years at around 9.5-10% pa as investor demand continues to chase the attractive yields on offer from commercial property. Industrial property has already run relatively hard so office and retail property are likely to outperform.

A-REITS having outperformed over the last few years are likely to go through a period of relative underperformance at some stage in the period ahead.

The key threats to keep an eye on would be a recession in the Australian economy and/or a sharp back up in bond yields. So far there is little sign of the former, with the economy continuing to gradually rebalance towards non-mining related activity, or the latter as global and Australian economic growth and inflation remain constrained.

By AMP Capital Markets 5 November 2015

About the Author

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.